%20Bold.png)

Mortgage advertising in the U.S. must follow strict rules to protect consumers and promote transparency. These regulations, enforced by the Consumer Financial Protection Bureau (CFPB) and Federal Trade Commission (FTC), ensure that lenders provide clear, accurate, and complete information in their ads. Non-compliance can lead to hefty fines or legal action. Here's what you need to know:

These rules aim to ensure fairness and clarity for borrowers while holding lenders accountable. Violations can result in fines up to $5,000 per day and even prison time. Compliance isn’t just about avoiding penalties - it builds trust and helps consumers make informed decisions.

The Annual Percentage Rate (APR) plays a key role in mortgage advertising. Unlike a standard interest rate, the APR gives borrowers a clearer picture of the true cost of borrowing by factoring in not just the interest, but also points, broker fees, and other prepaid finance charges. This makes it easier to compare loans directly. Federal regulations require this level of transparency.

According to Regulation Z (12 CFR § 1026.24), any mention of a finance charge in a mortgage ad must include the term "annual percentage rate" or its abbreviation, "APR".

If you choose to display a simple annual interest rate alongside the APR, the interest rate cannot be more prominent than the APR . For example, in 2021, a lender was cited for using a larger font for the interest rate compared to the APR.

"The interest rate may also be listed but not more conspicuously than the APR." – Allison Burns, Senior Examiner, Federal Reserve Bank of Minneapolis

For variable-rate mortgages, where the APR could increase, it’s crucial to clearly disclose this risk. Such disclosures must be presented in a way that is easy to understand and noticeable .

No-money-down offers are great at grabbing attention but come with strict rules to ensure they’re not misleading. According to 12 CFR § 1026.24(a), these claims must reflect actual credit terms available to consumers. This regulation is designed to prevent deceptive practices, like bait-and-switch tactics, and works hand-in-hand with the APR disclosure requirements discussed earlier.

Regulation N (12 CFR § 1014.3) explicitly forbids misleading statements about payments - whether it’s the existence, amount, number, or timing of payments. For example, if a no-money-down offer is offset by hidden fees, it’s not just unethical; it’s illegal under federal law and could also lead to state-level legal action.

Since no-money-down is considered a "triggering term" under 12 CFR § 1026.24(d), any advertisement making this claim must also clearly display the APR and full repayment terms. These details need to be just as noticeable as the no-money-down promise. In short, all credit terms in the ad must be accurate and transparent.

Before advertising such offers, ensure the loan program is genuinely available to qualified applicants. Avoid using absolute language if there are conditions or fees that might undermine the no-money-down claim.

Trigger leads are generated when a credit inquiry signals that a consumer is actively seeking a mortgage, which can alert competing lenders. Federal rules strictly regulate how this information can be used in mortgage advertising to ensure clarity and prevent deceptive practices.

Under Regulation Z (12 CFR § 1026.24(i)), if your advertisement mentions the name of a consumer's current mortgage lender, you must prominently display your company's name as well. Additionally, it's mandatory to clearly state that your company is not affiliated with the consumer's current lender. This ensures that consumers don't mistakenly believe the solicitation is from their trusted mortgage provider.

The regulation specifies:

"Using the name of the consumer's current lender in an advertisement that is not sent by or on behalf of the consumer's current lender [is prohibited], unless the advertisement: (i) Discloses with equal prominence the name of the person or creditor making the advertisement; and (ii) Includes a clear and conspicuous statement that the person making the advertisement is not associated with, or acting on behalf of, the consumer's current lender." - 12 CFR § 1026.24(i)

Regulation N further prohibits misleading claims about the source of the advertisement. This means you cannot use logos, design elements, or language that might falsely suggest government endorsement unless such claims are accurate.

Additionally, ensure that you advertise only credit terms that are genuinely available. Keep all records of trigger lead advertisements and related documentation for at least 24 months.

These regulations emphasize the importance of clear and accurate disclosures in mortgage advertising to protect consumers and maintain transparency.

Fair lending rules play a crucial role in ensuring consumer protection, especially when it comes to mortgage advertising. Beyond transparency requirements, fairness in lending is a cornerstone of compliance. The Equal Credit Opportunity Act (ECOA) mandates that mortgage advertisers provide equal access to credit for all qualified applicants, regardless of characteristics such as race, color, religion, national origin, sex, marital status, age, income derived from public assistance, or the exercise of rights under the Consumer Credit Protection Act. This legal framework reinforces the transparency highlighted in earlier disclosures.

When it comes to advertising, both written and visual materials must include the Equal Housing Lender logotype and legend. For oral advertisements, such as radio spots or spoken content in TV commercials, it’s essential to state that your institution is either an "Equal Housing Lender" or an "Equal Opportunity Lender". Ads must steer clear of any language, symbols, or imagery that could be interpreted as promoting discriminatory preferences. As outlined in 12 CFR § 338.3:

"No advertisement shall contain any words, symbols, models, or other forms of communication which express, imply, or suggest a discriminatory preference or policy of exclusion in violation of the provisions of the Fair Housing Act or the Equal Credit Opportunity Act."

To stay compliant, review all creative materials - images, wording, and scenarios - to ensure they don’t unintentionally suggest bias or exclusion of any group. Additionally, avoid misleading claims about a consumer's chances of being pre-approved or guaranteed for a mortgage, as such practices violate Regulation N and conflict with ECOA’s principles of fair lending.

Compliance isn’t limited to advertising. At physical loan offices, you must display a Fair Housing Poster (at least 11×14 inches) in a visible public area. Also, maintain records of all commercial communications for a minimum of 24 months to demonstrate adherence to federal non-discrimination laws.

When it comes to advertising mortgages, federal law demands that lenders stick to terms they’re actually prepared to offer. This rule, outlined in 12 CFR § 1026.24(a), is designed to prevent misleading practices, such as promoting enticing rates that are never intended to be available. As the regulation states:

"If an advertisement for credit states specific credit terms, it shall state only those terms that actually are or will be arranged or offered by the creditor."

This requirement complements the previously discussed trigger disclosures, ensuring that every advertised term is supported by a genuine offer.

Some details in mortgage ads, often referred to as "triggering terms", automatically require additional disclosures. These include mentions of the downpayment amount or percentage, the number of payments, specific payment amounts, or any finance charges. If these terms are included, the ad must also disclose the full downpayment, complete repayment terms, and the APR. If the APR is subject to change after closing or if the loan involves a balloon payment, these details must be clearly stated. When mentioning balloon payments, the disclosure must be just as prominent as any mention of minimum payments.

For ads that include payment amounts on loans secured by a first lien on a dwelling, it’s essential to clarify that the stated payments don’t include taxes and insurance premiums. This ensures borrowers understand that their actual payment obligations will be higher than the advertised amount.

Disclosures must be presented clearly and understandably. For printed materials, text must be easy to read. In broadcast ads, the information should be delivered at a pace and volume that the audience can follow. For internet ads, a direct link to a table containing additional disclosures is acceptable.

Regulation N takes this a step further by prohibiting material misrepresentation of loan terms. This includes misleading statements about fees, prepayment penalties, or falsely claiming a rate is "fixed" when it isn’t. If a rate is fixed for only a limited time, the ad must specify the exact duration and note that the rate could increase afterward. Additionally, while a simple annual interest rate can be displayed alongside the APR, it must not overshadow the APR in prominence or visibility.

Making the principal broker's identity clear is essential for maintaining transparency in mortgage advertising. Federal law ensures that every mortgage ad must plainly state the loan provider’s identity to avoid misleading consumers.

Regulation N (12 CFR 1014.3) strictly forbids any misrepresentation about the source of a commercial communication. In simple terms, advertisements cannot falsely suggest they are tied to a consumer's current mortgage lender or servicer. The regulation clarifies:

"It is a violation of this part for any person to make any material misrepresentation, expressly or by implication, in any commercial communication, regarding... the source of any commercial communication, including but not limited to misrepresentations that a commercial communication is made by or on behalf of the consumer's current mortgage lender or servicer."

Additionally, lenders are prohibited from creating the impression that they are affiliated with government entities. This includes using designs, logos, or symbols that mimic official government correspondence, which could mislead consumers into thinking the lender is endorsed or sponsored by a government program.

To ensure compliance, always include the full legal name of the principal broker or lender in your advertisements. Regulation Z also requires the creditor's address to be provided. If the lender has not been determined at the time of the ad, this information should be disclosed as soon as possible. Many states impose even stricter requirements, often mandating the inclusion of the broker's license number in all ads. Be sure to check your state-specific regulations to avoid any compliance issues.

In addition to providing detailed term disclosures, lenders must also clearly communicate the risks tied to specific mortgage offers. Mortgage ads are required to include straightforward risk warnings - especially for high-cost loans and products involving private mortgage insurance (PMI). This ensures borrowers fully grasp the financial stakes involved.

For high-cost mortgages, federal law requires a specific warning to be prominently displayed in advertisements:

"If you obtain this loan, the lender will have a mortgage on your home. You could lose your home, and any money you have put into it, if you do not meet your obligations under the loan."

If your ad includes a specific payment amount for a first-lien mortgage, you must disclose that this figure does not include costs like property taxes, homeowners insurance, or PMI premiums. Since these additional expenses will increase the total monthly payment, this disclaimer must be placed visibly near the advertised payment amount - not hidden in fine print at the bottom of the page.

When it comes to private mortgage insurance, it’s important to highlight the differences between borrower-paid and lender-paid options. Borrower-paid PMI can typically be canceled once the homeowner’s equity reaches 20% (loan-to-value ratio of 80%) and is automatically canceled when equity hits 22% (78% LTV). In contrast, lender-paid mortgage insurance (LPMI) cannot be canceled, and these loans often come with higher interest rates.

Regulation N also strictly forbids misleading claims about default scenarios. For example, you cannot misrepresent situations that could lead to a default, such as failing to pay taxes, insurance, or maintain the property. Additionally, avoid labeling any variable-rate loan as "fixed", as this could mislead consumers about the nature of their loan terms.

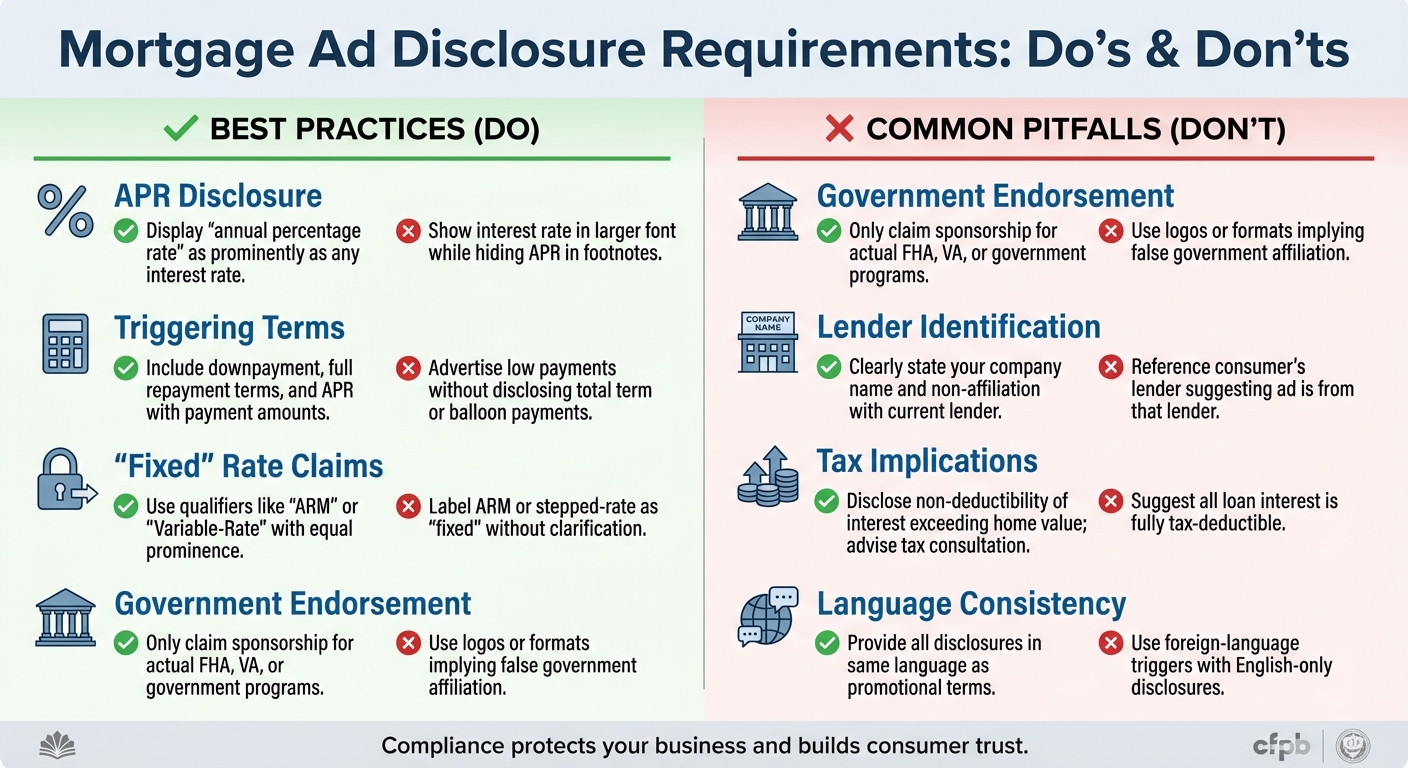

Mortgage Advertising Disclosure Requirements: Best Practices vs Common Pitfalls

The table below highlights key disclosure practices and contrasts them with common missteps, offering a quick guide to navigating regulatory requirements effectively.

| Requirement | Best Practice | Common Pitfall |

|---|---|---|

| APR Disclosure | Clearly spell out "annual percentage rate" and ensure it is displayed as prominently as (or more than) any simple interest rate. | Display a simple annual interest rate in a larger or bolder font, while relegating the APR to a footnote. |

| Triggering Terms | Include downpayment details, full repayment terms, and APR whenever a specific payment amount is mentioned. | Advertise low monthly payments without disclosing the total repayment term or balloon payments. |

| "Fixed" Rate Claims | Use qualifiers like "ARM", "Adjustable-Rate Mortgage", or "Variable-Rate Mortgage" alongside "fixed" with equal prominence. | Label an ARM or stepped-rate mortgage as "fixed" without proper clarification. |

| Government Endorsement | Only claim sponsorship for FHA, VA, or other government-backed programs. | Use logos, names, or formats that imply false government affiliation or endorsement. |

| Lender Identification | Clearly state your company name and disclose that you are not affiliated with a consumer's current lender, with equal prominence. | Reference a consumer’s current lender in a way that suggests the ad is directly from that lender. |

| Tax Implications | Inform consumers that interest on credit exceeding the home’s fair market value is not tax-deductible, and advise consulting a tax advisor. | Suggest that all loan interest, even on amounts exceeding the home’s value, is fully tax-deductible. |

| Language Consistency | Ensure all required disclosures appear in the same language as the promotional "trigger" terms. | Use foreign-language trigger terms but provide required disclosures only in English. |

This comparison underscores the importance of adhering to clear and conspicuous disclosure practices.

Additionally, keep disclosure data like index and margin information updated - every 60 days for direct mail and every 30 days for electronic ads - to remain compliant. Avoid misleading terms like "counselor" for for-profit brokers, and steer clear of claims that a mortgage will "eliminate" or "forgive" debt.

Staying compliant with mortgage advertising rules isn't just a legal requirement - it’s essential for protecting your business from hefty fines and reputational damage. In 2023 alone, penalties ranged from $1.75 million to $12 million, with violations under the Truth in Lending Act (TILA) carrying fines of up to $5,000 and even the possibility of up to one year in prison.

"If your real estate or mortgage-related business is within the jurisdiction of the FTC, it's important to see to it that your advertising, marketing materials, and day-to-day practices meet legal standards."

– Federal Trade Commission

Beyond avoiding penalties, compliance helps build trust with consumers. It ensures borrowers can accurately compare credit terms, which fosters transparency and encourages repeat business.

The examples highlighted here show how crucial it is to maintain strict compliance across all advertising platforms. With multiple regulatory agencies enforcing these standards, mortgage brokers and financial services leaders must prioritize clear and consistent disclosures across every channel. This approach not only protects your business but also strengthens consumer confidence.

Moreover, effective disclosure practices do more than meet legal requirements - they can drive business growth. Tools like Visora support financial leaders by simplifying compliance tasks and improving acquisition strategies. By automating trigger term detection, standardizing APR visibility, and ensuring accurate recordkeeping, businesses can focus on sustainable growth while maintaining regulatory integrity. This allows for building reliable revenue streams without resorting to risky shortcuts.

Failing to follow mortgage ad disclosure rules can lead to serious repercussions. Agencies such as the Federal Trade Commission (FTC) and the Consumer Financial Protection Bureau (CFPB) have the authority to impose civil penalties, fines, or even pursue legal action. Beyond financial consequences, businesses could suffer reputational harm or be forced to overhaul their advertising strategies to align with compliance standards.

To steer clear of these pitfalls, businesses must prioritize creating mortgage advertisements that are clear, truthful, and fully compliant with disclosure regulations. Transparency and accuracy aren't just legal requirements - they're essential for maintaining trust.

The Equal Credit Opportunity Act (ECOA) plays a key role in promoting fairness in mortgage advertising. It specifically prohibits the use of discriminatory language, ensuring that lenders do not suggest credit decisions are influenced by factors such as race, color, religion, national origin, sex, marital status, age, or whether an applicant receives public assistance.

Moreover, the ECOA requires lenders to provide clear explanations for credit denials if applicants request them. This level of transparency is designed to ensure equal access to credit for all individuals.

To meet regulatory standards, mortgage advertisements must display only credit terms that can genuinely be offered while ensuring the information is presented clearly and prominently. They must include the annual percentage rate (APR), highlight any potential rate increases after the loan is finalized, and provide extra disclosures if details such as loan amount, payment terms, or loan duration are specified. These measures are essential for avoiding misleading or deceptive claims.

%20(5).png)