%20Bold.png)

CRM systems are transforming compliance in financial services. They simplify regulatory processes, reduce errors, and improve efficiency by embedding compliance features directly into workflows. Here's how they help:

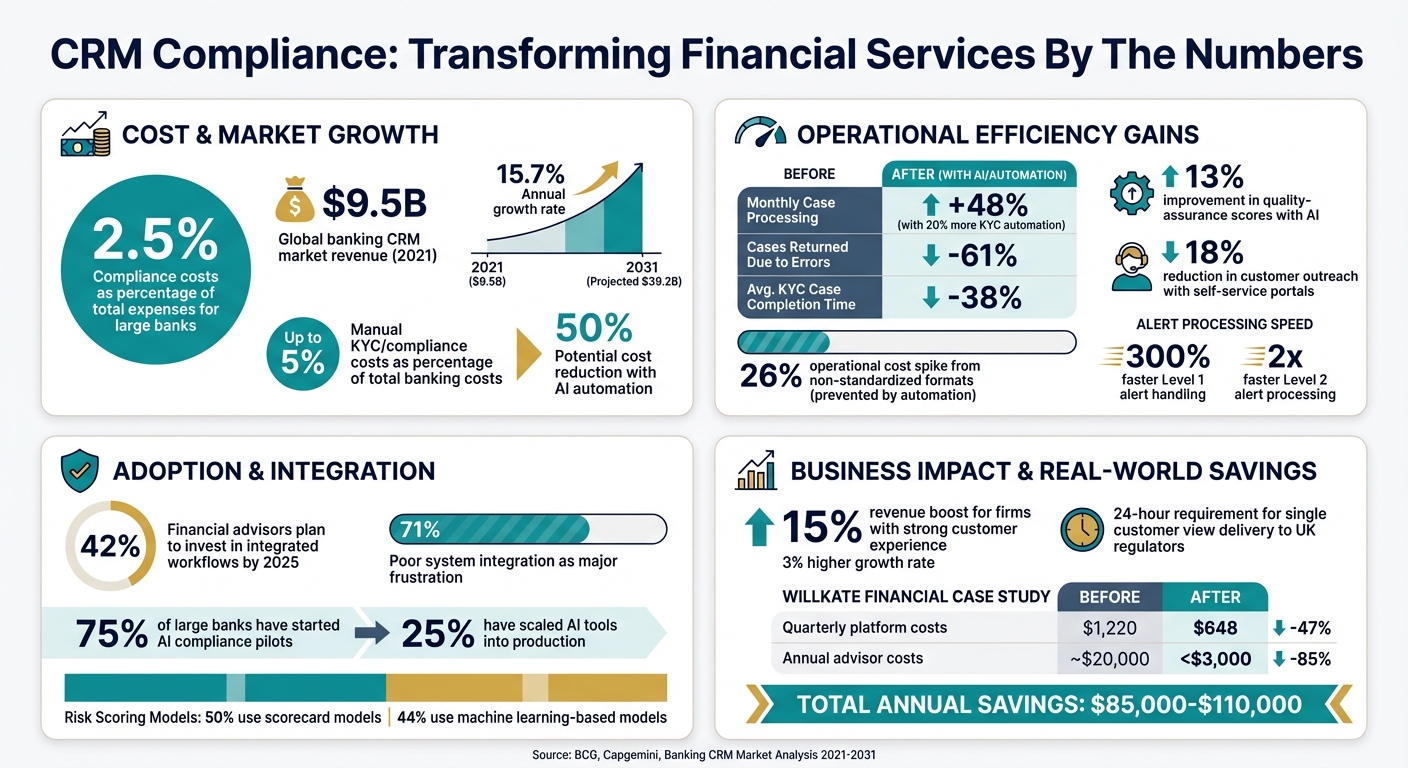

With compliance costs consuming up to 2.5% of total expenses for large banks, CRM systems offer a practical way to manage these challenges while building trust and improving operations.

CRM Compliance Impact: Key Statistics for Financial Services

CRM platforms are no longer just tools for managing customer relationships - they’ve become essential for regulatory compliance. Financial services firms face growing demands to meet reporting requirements, such as those outlined in the EU’s Digital Operational Resilience Act (DORA). The real challenge lies in quickly and accurately unifying data from outdated systems [3]. By embedding compliance capabilities directly into their frameworks, CRM systems are transforming how firms manage these requirements, paving the way for smoother operations.

With AI-powered automation, CRM systems take the headache out of regulatory reporting. These platforms eliminate tedious manual data entry, saving time and reducing errors [3]. Automated data reconciliation ensures traceability and consistency, which is especially useful for responding to unexpected regulator requests at lightning speed [3]. Real-time alerts detect compliance issues almost instantly - critical for services like instant payments [3].

Take deposit insurance regulations in the UK, for example. Banks are required to maintain a single customer view that can be delivered to regulators within 24 hours to process claims [3]. CRM systems streamline this process by unifying data across multiple channels, ensuring compliance at every step of the customer journey [3]. Tasks that once took hours or even days can now be completed in seconds, a game-changer for risk and compliance management [3].

CRM systems automatically log and time-stamp every client interaction, creating a transparent record that simplifies regulatory reviews [4][7]. Role-based access controls (RBAC) ensure only authorized personnel can view sensitive client data, helping firms stay compliant with privacy laws like GDPR and CCPA [4][5]. Additionally, data encryption safeguards information whether it’s stored or being transmitted, and consent management tools help track and manage customer permissions effectively [5].

"A CRM gives you the infrastructure now that will support your success later in any future audits."

- Cameo Roberson, CEO and Founder, Atlas Park Consulting [7]

These automated audit trails eliminate the risks of relying on unstructured formats like Excel spreadsheets [6]. Features like document tracking and secure storage ensure all regulatory paperwork - such as KYC files and loan applications - is properly managed and easily accessible [4][7]. This level of organization supports compliance while also aligning with broader operational goals. The numbers back this up: the global banking CRM market, which brought in $9.5 billion in revenue in 2021, is projected to grow at a 15.7% annual rate, reaching $39.2 billion by 2031. Much of this growth is driven by the compliance and security features these systems provide [6].

Modern CRM systems act as central hubs, connecting billing, trading, and compliance data. Open APIs enable seamless integration with specialized RegTech tools, eliminating the need for manual data entry. This creates a unified ecosystem where compliance monitoring works as a cohesive system. Such integration is critical for meeting "Single-Customer View" requirements, allowing firms to track customer activity across their entire lifecycle and across business units, as regulators now expect.

The benefits are clear: 42% of financial advisors plan to invest in integrated workflows by 2025, while 71% cite poor system integration as a major frustration and operational risk [8]. A case in point is WillKate Financial, which partnered with Revisor in October 2025 to overhaul its fragmented tech stack. By replacing its Tamarac license and implementing global rebalancing, the firm cut quarterly platform costs from $1,220 to $648 and reduced advisor-paid costs from around $20,000 to under $3,000 annually. This resulted in total savings estimated between $85,000 and $110,000 per year [8].

"Technology that enhances agility in navigating this [regulatory] environment is increasingly a source of competitive differentiation."

- Bryan Comis, Jeanne Kwong Bickford, Benjamin Rehberg, Anne Kleppe, and Marianna Leoni, BCG [3]

Incorporating compliance features directly into CRM systems enhances operational workflows, allowing businesses to scale efficiently without incurring extra expenses [1]. This shift from reactive, "check-the-box" compliance to proactive, built-in systems is reshaping how teams manage tasks like client onboarding and ongoing relationship management. These advancements underscore the importance of integrating compliance tools into CRM platforms to meet strict regulatory requirements.

Embedding compliance processes into CRM workflows ensures consistency, significantly cutting down on errors. For example, banks that automated just 20% more of their end-to-end KYC (Know Your Customer) processes reported a 48% increase in monthly case processing [10]. Streamlined workflows and fewer hand-offs between teams also led to a 61% drop in cases returned due to errors [10].

Operational costs can spike by 26% due to non-standardized formats and duplicate data entries [10]. Automated systems help by validating data as it’s entered, ensuring consistency and reducing these unnecessary costs [9]. Additionally, AI-powered quality control systems independently verify compliance tasks, improving quality-assurance scores by 13% [10].

Traditional KYC processes are often slow and labor-intensive, requiring relationship managers to track down documents and manually verify information. Modern CRM systems transform this approach with automation. Algorithms now handle identity verification, eliminating the need for human intervention during due diligence [2]. This has cut the average time to complete a KYC case by 38% [10].

The financial benefits are equally compelling. Manual KYC and compliance tasks can account for up to 5% of total banking costs, but leveraging AI in these processes can reduce those costs by as much as 50% [9]. Intelligent alert handling systems further enhance efficiency by grouping related compliance alerts, assigning risk scores, and automatically closing low-risk cases while escalating high-risk ones [1]. Early adopters have seen Level 1 alert handling speeds triple and Level 2 handling double [1].

Self-service portals also play a crucial role, allowing clients to upload documents directly. This reduces customer outreach by 18% and increases processing capacity [2][10]. These improvements are particularly valuable for firms focused on customer experience - financial institutions with strong customer-experience ratings see a 15% boost in revenue and a 3% higher growth rate [10].

Managing compliance across multiple disconnected systems often leads to inefficiencies and regulatory gaps. A unified CRM platform eliminates these issues by consolidating all client data into a single, integrated source [2]. This "golden record" approach ensures that information is neither duplicated nor lost, enabling firms to perform due diligence and maintain a complete view of each customer throughout their lifecycle [2].

"A single unified solution that handles all KYC/AML requirements renders the entire compliance endeavor more effective and prevents information from being either not sufficiently communicated or inefficiently replicated."

The benefits extend beyond compliance. When relationship managers can access comprehensive client histories in one place, they spend less time searching for data and more time focusing on meaningful client interactions. Real-time data governance further ensures that all data categories are well-organized, with clear roles for stewardship and high-quality data feeds from both internal and external sources [10][2]. This integrated approach turns onboarding into an ongoing process of "lifestyle management", maintaining a holistic view of customer relationships [2]. By uniting compliance and operational workflows, firms not only improve day-to-day efficiency but also strengthen their overall regulatory stance.

Modern CRM tools are reshaping how financial firms approach compliance, turning it from a tedious obligation into a strategic advantage. These systems go far beyond simple contact management, offering features that streamline workflows, enhance compliance efforts, and even open doors for business opportunities. However, there's a gap in adoption - while 75% of large and regional banks have started AI and GenAI compliance pilots, only 25% have successfully scaled these tools into production [1]. This highlights the need for CRM systems with proven and reliable capabilities.

AI-driven CRM systems are game-changers when it comes to detecting compliance risks. Using machine learning, these tools can identify money-laundering patterns and improve how alerts are managed, significantly cutting down on false positives. For instance, 50% of financial institutions are already leveraging scorecard models that assign risk scores to alerts, while 44% have implemented machine learning-based models [1].

Automation plays a key role here, speeding up Level 1 alert handling by 300% and doubling the efficiency of Level 2 processes [1]. These systems group related alerts, assign risk levels, and use techniques like "hibernation" to filter out low-priority cases. AI-powered network analysis adds another layer of insight, uncovering hidden connections between entities - a critical capability for spotting bad actors who hide behind complex shell companies.

"AI and GenAI are powerful tools for compliance functions, but only when used with the right controls and governance." - Boston Consulting Group [1]

The analytics capabilities of a CRM system need to do double duty: meeting regulatory requirements while also driving strategic business decisions. For example, graph analytics can untangle complex Ultimate Beneficial Ownership (UBO) structures and calculate ownership percentages across various legal entities [11]. Network analysis tools go further, mapping out financial crime patterns while also identifying legitimate business relationships - useful for cross-selling and understanding market influence.

Advanced analytics blend structured CRM data with unstructured sources like adverse news and social media feeds. This combination supports due diligence efforts while also fueling business development [11]. With global systemically important banks (G-SIBs) spending up to 2.5% of their total costs on second-line compliance functions [1], efficient analytics are essential to justify these investments. The right CRM system can reduce operational burdens while improving both compliance and business intelligence.

For financial firms, CRM systems must integrate seamlessly with existing tools and scale to meet growing needs. Disconnected KYC processes, for example, are not only inefficient but also prone to costly errors. As Manish Chopra, Executive Vice President at Capgemini, notes, managing such processes without coordination is "costly, inefficient, and error-prone" [11]. Consolidating IT platforms for tasks like risk ranking, PEP screening, and UBO identification helps eliminate data silos and cuts down on duplicate efforts.

Low-code workflow orchestration platforms are another essential feature, allowing non-technical staff to update and manage compliance processes without constant IT support [1]. This flexibility is crucial as regulations evolve, such as the EU's Anti-Money Laundering package coming in July 2024 and the EU AI Act in August 2024 [1]. G-SIBs, which spend a median of 26% of their compliance budgets on IT compared to 11% for regional banks [1], need systems that can grow with their business without requiring expensive overhauls. By focusing on scalability and integration, firms can better navigate the ever-changing regulatory landscape.

Financial services firms are constantly navigating a maze of evolving regulations, data security threats, and intricate reporting requirements. Modern CRM platforms step up to the plate by weaving compliance directly into daily workflows, addressing these challenges head-on. These systems build upon the automated compliance and operational improvements already discussed. As BCG aptly puts it, "Firms that can nimbly adapt to regulatory changes can retain their focus on growth, customer experience, and other strategic initiatives; those that struggle to do so must dedicate ever-increasing time and resources to compliance activity" [3]. By embedding compliance features, these platforms not only meet regulatory standards but also streamline operations, paving the way for a deeper dive into their capabilities.

Keeping up with shifting regulations is no small feat, especially given the frequent updates in major jurisdictions. CRM platforms designed with compliance-by-design principles make this process much smoother. With low-code orchestration tools, compliance teams - without needing technical expertise - can tweak workflows to align with new rules, eliminating delays caused by waiting for IT support [1]. These platforms also offer a "common core" architecture, which can be tailored to meet region-specific requirements, such as GDPR in Europe or India’s Digital Personal Data Protection Act of 2023 [3]. This modular setup spares firms from the headache and expense of overhauling outdated systems, ensuring they stay agile and compliant.

Safeguarding sensitive client data goes far beyond basic password protection. Modern CRM systems employ granular permissions management, allowing firms to control exactly who can access or edit specific customer details [3]. They also use advanced tagging to comply with data localization laws, tracking residency requirements and retention limits [3].

The importance of data protection is clear: 71% of financial institutions now consider it a core part of their compliance efforts [1]. CRM platforms enhance this by providing complete data lineage, which tracks the origin and access history of customer information across systems [2]. This "golden record" is invaluable during regulatory audits, offering full traceability. Automated data reconciliation frameworks ensure consistency, enabling firms to respond to audits with speed and accuracy [3]. For those leveraging AI within their CRM, ongoing monitoring tackles risks like model drift or unintended bias, safeguarding data integrity [1].

Beyond securing data, CRM platforms also take the hassle out of compliance documentation. They can automatically populate SARs and other required forms, slashing processing times and minimizing errors [1].

Unified customer records make regulatory reporting faster and more precise, meeting increasing demands for transparency in areas like deposit insurance and beneficial ownership [3][2]. Centralized GRC tools integrated into CRMs provide a one-stop shop for retrieving evidence, offering real-time snapshots of compliance status during audits [12]. Early adopters of automated alert processing have seen impressive results: Level 1 alerts are now handled 300% faster, while Level 2 processing speeds have doubled [1]. These time savings allow compliance teams to focus on critical tasks instead of being bogged down by paperwork.

Financial services firms face a choice: treat compliance as a necessary burden or turn it into a strategic advantage. The data makes a compelling case for the latter. CRM systems that integrate compliance not only meet regulatory requirements but also simplify operations. As BCG puts it, "Banks that embrace integrated risk management, compliance by design, and AI and GenAI adoption will redefine compliance as a strategic enabler rather than a regulatory burden" [1]. This isn't just about avoiding penalties, which averaged $145.33 million in 2019 [13]. It's about creating a foundation for long-term growth.

The operational benefits of embedding compliance into CRM workflows are hard to ignore. Firms that take this approach eliminate costly manual rework, speed up client onboarding with automated KYC processes, maintain audit-ready records without last-minute scrambles, and scale operations without proportionally increasing costs or staff. These efficiencies free up resources, allowing firms to focus on growth rather than firefighting compliance issues.

Reframing compliance as a driver of business resilience rather than a cost center marks a significant shift for leading institutions [1]. When compliance tools are seamlessly integrated into daily workflows instead of being tacked on as an afterthought, firms gain the flexibility to adapt to new regulations, maintain a unified customer view that regulators increasingly demand, safeguard sensitive data with advanced controls, and respond to audits with full traceability. In an environment where agility is a competitive edge, technology that supports this adaptability is becoming a key differentiator [3]. The gap between firms that embrace these tools and those that lag behind continues to grow.

This conclusion ties together themes of automation, standardized workflows, and AI-driven risk management. For financial services leaders, the question isn't whether to adopt compliance-focused CRM systems - it’s how quickly they can implement them. Early adopters aren't just meeting regulatory requirements; they’re gaining a competitive edge that compounds over time. By optimizing CRM systems with compliance at their core, firms not only stay ahead of regulations but also transform compliance into a growth engine, turning what was once a limitation into a powerful advantage.

CRM systems are essential for financial services firms aiming to stay on top of compliance requirements. By centralizing client data, automating repetitive tasks, and maintaining accurate records, these systems simplify the complex process of meeting regulatory standards. Features like audit trails, real-time monitoring, and role-based access controls play a key role in minimizing compliance risks and ensuring transparency.

Beyond compliance, CRMs help financial firms work smarter. They streamline workflows and provide detailed reporting, which not only supports regulatory adherence but also boosts overall efficiency. This means firms can save both time and resources while maintaining a strong focus on operational excellence.

AI takes the hassle out of CRM compliance by turning a traditionally manual and time-intensive process into a streamlined, proactive system. With tools like optical character recognition (OCR) and natural language processing, AI automates tasks such as data extraction, slashes error rates, and speeds up onboarding. It keeps a constant eye on transactions and client profiles, ensuring they meet the latest regulatory standards. Plus, it flags potential issues in real time, helping businesses address problems before they result in costly penalties.

AI-powered CRM systems also bring advanced features like dynamic risk scoring and automated audit trails. These tools give compliance officers a clear, consolidated view of regulatory adherence throughout the client lifecycle. The result? Fewer repetitive manual checks, lower operating costs, and seamless compliance with standards like Know-Your-Customer (KYC) and anti-money-laundering (AML). By integrating these capabilities directly into workflows, financial firms can stay compliant while dedicating more energy to nurturing client relationships and driving growth.

CRM systems play a key role in strengthening data security for financial services firms by consolidating client and transaction data into a single, secure platform. This eliminates the risks tied to outdated or scattered records, offering better protection for sensitive information.

Modern CRMs come equipped with role-based access controls, ensuring only authorized personnel can view or modify specific data. They also maintain detailed audit logs to track user activity, which enhances traceability and simplifies compliance reporting. Features like encrypted data storage and automated compliance checks help firms stay aligned with regulatory standards, such as those set by the SEC and FINRA, while reducing the need for manual monitoring.

By securely integrating with financial tools like QuickBooks or Stripe through APIs, CRMs also minimize exposure to third-party breaches. These advanced security measures allow financial firms to protect client information, prevent data breaches, and confidently meet regulatory requirements.

%20(5).png)