%20Bold.png)

Referral programs can be a powerful tool for financial firms to attract new clients through trusted recommendations. However, strict regulations from agencies like the SEC, FINRA, and CFPB require firms to prioritize transparency and compliance. Here's what you need to know:

Following these guidelines ensures your referral program remains compliant while building trust with clients.

Financial Referral Program Regulatory Requirements by Agency and Firm Type

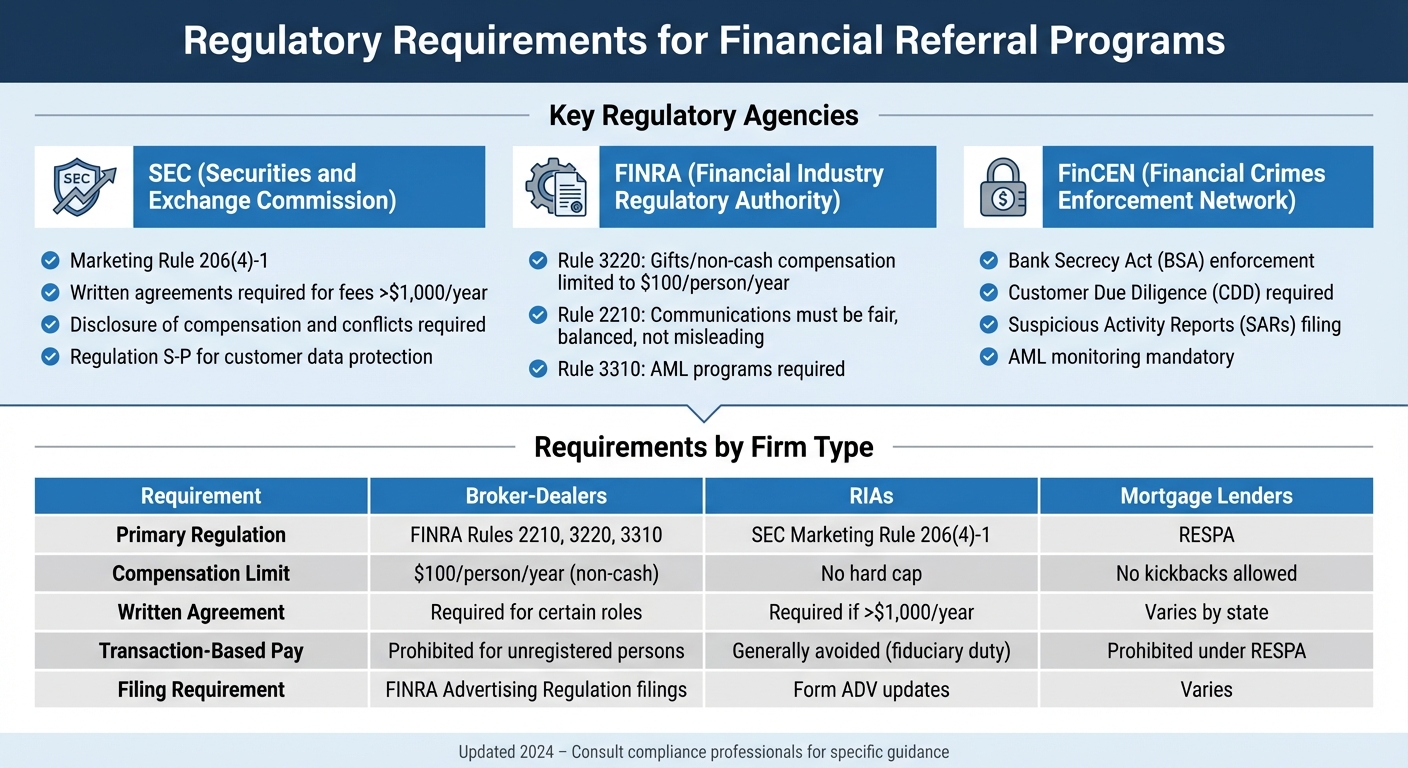

When it comes to financial referral programs, three key agencies play a major role in ensuring compliance: the SEC, FINRA, and FinCEN. Understanding their rules is critical to avoid steep penalties.

The SEC (Securities and Exchange Commission) enforces the Marketing Rule (Rule 206(4)-1) for Registered Investment Advisors. This rule mandates transparency about referral payments, potential conflicts of interest, and the relationship between the firm and the referrer. If a firm pays more than $1,000 in referral fees over 12 months, a written agreement is required [1].

FINRA (Financial Industry Regulatory Authority) regulates broker-dealers with several important rules. Rule 2210 requires all public communications to be fair, balanced, and not misleading [3]. Rule 3220 limits gifts and non-cash compensation to $100 per individual per year to prevent undue influence [1]. Additionally, Rule 3310 ensures firms have robust Anti-Money Laundering (AML) programs in place, especially to monitor accounts opened through referrals [7].

FinCEN (Financial Crimes Enforcement Network) enforces the Bank Secrecy Act (BSA), which requires financial firms to implement AML programs, conduct Customer Due Diligence (CDD), and file Suspicious Activity Reports (SARs) for transactions that might involve fraud or money laundering [6][7].

"FinCEN is committed to being transparent about its approach to BSA enforcement. It is not a 'gotcha' game. The information required by the BSA saves lives, and protects our communities and people from harm. It is a national security issue." – Kenneth A. Blanco, Director, FinCEN [6]

The SEC's Regulation S-P sets strict rules for protecting customer nonpublic information (NPI). Firms must provide privacy notices and opt-out options before sharing any data with third-party referrers [5]. For mortgage lenders, the Real Estate Settlement Procedures Act (RESPA) prohibits kickbacks or unearned fees for referrals [1].

| Agency | Key Rule | Referral Program Requirement |

|---|---|---|

| SEC | Marketing Rule 206(4)-1 | Disclose compensation and have written agreements for fees above $1,000 |

| FINRA | Rule 3220 | Limit gifts/non-cash compensation to $100 annually per person |

| FINRA | Rule 2210 | Ensure promotional materials are fair, balanced, and not misleading |

| FinCEN | Bank Secrecy Act (BSA) | Implement AML monitoring and Customer Identification Programs |

These rules create the backbone for regulatory compliance, but staying updated on changes is equally important.

Recent updates have further tightened compliance requirements for referral programs. Starting October 1, 2024, the National Automated Clearinghouse Association (Nacha) will require all non-consumer participants in the ACH network to establish fraud detection and monitoring systems [7]. This shift is significant because ACH fraud has been the most reported suspicious activity in securities and futures SAR filings between 2014 and 2022 [7].

Regulators are also increasing scrutiny of identity verification processes, especially for accounts opened through referral links. Firms are under pressure to address "instant funds abuse", where customers attempt to fraudulently reclaim funds after receiving immediate credit from brokerage firms [7].

FINRA has begun reviewing how firms use social media influencers in referral programs. These reviews focus on whether firms have adequate Written Supervisory Procedures (WSPs) to manage influencer compensation and ensure compliance. This includes distinguishing standard referral programs from those involving high-profile influencers [5].

Another emerging concern is adversarial AI. Fraudsters are leveraging generative AI to create deepfake content that mimics financial experts in "investment club" scams promoted via social media referral channels [7]. In response, regulators are emphasizing stronger identity verification measures, such as "likeness checks", which compare live photos or videos to official ID documents [7].

The SEC Marketing Rule continues to require full disclosure of referral compensation and any conflicts of interest, particularly when referrers may have a financial stake in their recommendations [1].

Understanding these updates is critical, but so is avoiding common compliance mistakes.

Despite clear regulatory guidance, firms often make avoidable missteps when managing referral programs.

One frequent error is failing to disclose referral compensation, conflicts of interest, or the nature of the relationship with the referrer. The SEC Marketing Rule requires these disclosures for any compensated referral arrangement [1].

Another common violation is paying transaction-based compensation to unregistered individuals. Under Section 15 of the Securities Exchange Act, fees tied to the number or value of transactions require the recipient to be a registered broker [1].

AML lapses are also a major issue. Firms must conduct risk-based Customer Due Diligence on referred accounts and monitor for red flags like sudden large withdrawals, mismatched IP addresses, or abrupt account activity changes [7]. FINRA Rule 3310(c) mandates annual independent testing of AML programs to ensure they effectively capture suspicious activities tied to referrals [7].

Social media and influencer programs can pose compliance risks if firms lack adequate Written Supervisory Procedures. Regulators expect WSPs to address influencer compensation, require background checks on social media activity, and mandate ongoing monitoring of communications for compliance [5].

Another pitfall is failing to archive and review communications from third-party referrers. FINRA Rule 2210 requires firms to capture, review, and approve all promotional materials created by referral partners to ensure they are fair and not misleading [3].

Finally, creating high-pressure referral incentives can lead to violations of UDAAP (Unfair, Deceptive, or Abusive Acts or Practices) standards under the Consumer Financial Protection Act. Incentives that push borrowers toward unsuitable products or create undue urgency can breach consumer protection laws [1].

The way you reward referrers directly impacts which regulations apply to your program. For broker-dealers, FINRA Rule 3220 imposes strict limits, allowing only up to $100 in non-cash compensation per individual annually [1]. Offering higher-value non-cash rewards can lead to compliance violations.

Registered Investment Advisors (RIAs) operate under the SEC Marketing Rule, which requires a written agreement for referrers earning more than $1,000 in total compensation over a 12-month period [1]. For compensation under this threshold, simpler agreements may suffice, provided the referral relationship is clearly disclosed to clients.

Transaction-based compensation is another area to tread carefully. According to Section 15 of the Securities Exchange Act of 1934, paying unregistered individuals a percentage of trades or transactions is prohibited. This means referrers must hold broker registrations to receive such payments [1]. Avoiding transaction-based payouts for unregistered individuals is a must.

"Under the SEC Marketing Rule, RIAs must enter into a written agreement with any person or entity that receives cash or non-cash compensation for providing a testimonial, endorsement, or client referral." – InnReg [1]

For mortgage lenders, the Real Estate Settlement Procedures Act (RESPA) bans kickbacks and unearned fees for referrals [1]. Instead, you might consider flat-fee arrangements for legitimate marketing services that steer clear of conflicts of interest.

Here’s a quick comparison of regulatory requirements:

| Firm Type | Compensation Limit | Written Agreement Required | Transaction-Based |

|---|---|---|---|

| Broker-Dealers | $100 per person per year | Required for certain roles | Prohibited for unregistered persons |

| RIAs | No hard cap | Required if compensation exceeds $1,000 annually | Generally avoided due to fiduciary duty |

| Mortgage Lenders | No kickbacks allowed | Varies by state | Prohibited under RESPA |

When creating your compensation model, steer clear of aggressive incentives that might encourage unsuitable recommendations. Such practices could fall under scrutiny for violating UDAAP (Unfair, Deceptive, or Abusive Acts or Practices) standards.

Next, let’s look at who can participate in your referral program.

Eligibility rules are just as critical as compensation guidelines for staying compliant. The SEC Marketing Rule prohibits compensating "bad actors" - individuals disqualified due to certain Commission orders or felony convictions [9]. Conducting thorough background checks is essential before onboarding referrers.

Most financial referral programs rely on existing clients, professional partners, and affiliates. For RIAs, if a professional partner earns more than $1,000 annually in compensation, they must sign a written agreement detailing their promotional activities and payment terms [1].

Social media influencers demand extra attention. It’s vital to perform background checks and review their online activity to identify any potential compliance or reputational risks [5]. This includes verifying they have no past regulatory violations and ensuring they understand the boundaries of what they can and cannot say about your services.

"The rule prohibits certain 'bad actors' from acting as promoters for compensation, subject to exceptions where other disqualification provisions apply." – SEC Small Entity Compliance Guide [9]

For money transmitters and payment fintechs, identity verification is key. Participants should undergo customer due diligence and provide government-issued IDs to minimize fraud risks.

It’s also crucial to define prohibited behaviors in your program terms. Clearly state that referrers cannot exaggerate claims, omit necessary disclosures, or misrepresent your services. Regular monitoring of social media and other communications can help catch and address compliance issues early.

Proper management is vital to ensure compliance while maintaining smooth operations. Keep detailed records of all referral agreements, compensation details, and communications to meet regulatory obligations. For instance, SEC and FINRA require firms to archive communications related to referral and influencer activities [5].

Using compliance automation tools can simplify this process. These tools help centralize tracking, manage written agreements, monitor payments against regulatory limits, and archive promotional materials. This ensures you stay within thresholds like the SEC's $1,000 limit or FINRA's $100 gift cap without missing documentation.

Develop Written Supervisory Procedures (WSPs) specifically for your referral program. These should outline how compensation is managed, differentiate between standard referrers and influencers, and include steps for responding to regulatory updates. Regularly updating these procedures keeps them aligned with new rules [5].

Training is another critical component. Offer targeted training sessions for both internal staff and external referrers. Cover topics such as acceptable practices, disclosure requirements, and how to identify and avoid misleading claims.

Finally, ongoing monitoring is key to keeping your referral program compliant. Review referrer communications regularly, analyze conversion rates to spot unusual trends, and audit compensation payments periodically. Implement a pre-approval process for social media content to ensure all promotional messaging is accurate and fair.

Transparency begins from your very first interaction with a client. It’s essential to clearly communicate if the person making a referral is a current client of your firm and whether they’re receiving any form of compensation. This could include cash payments, fee reductions, or brokerage incentives [9][10].

You should also outline the compensation terms in detail so clients know exactly how much the referrer is being paid and the nature of the arrangement between your firm and the promoter [9][10]. Any potential conflicts of interest tied to referrals must be disclosed upfront [11].

For broker-dealers operating under Regulation Best Interest, disclosures must go further. They need to cover material fees and costs tied to the client’s transactions and accounts, as well as the type and scope of services being offered [11]. This ensures clients are fully informed about any limitations on the securities or strategies being recommended.

"Advertisements must clearly and prominently disclose whether the person giving the testimonial or endorsement (the 'promoter') is a client and whether the promoter is compensated." – SEC [9]

Disclosures should be both clear and visible within your marketing materials or provided at the time of the referral [9][10]. If you’re making oral disclosures to meet Regulation Best Interest requirements, you must maintain records to prove these disclosures were delivered [11].

These practices set the stage for consistent documentation and compliance in recordkeeping.

Registered Investment Advisors (RIAs) are required to update their Form ADV filings to include details about their marketing practices, particularly those involving compensated testimonials and endorsements [9]. This filing keeps the SEC informed about your referral practices and ensures regulatory compliance.

If a promoter earns more than $1,000 in total compensation within a 12-month period, a written agreement must be in place. This agreement should define the scope of their activities and payment terms [1][10]. For compensation below this threshold, while a written agreement isn’t mandatory, it’s still necessary to document the arrangement internally [1][9].

Under Rule 204-2, firms are required to maintain records of all marketing materials, including oral testimonials and endorsements [9]. Using centralized documentation systems can simplify internal audits and regulatory reviews by keeping agreements, compensation records, and marketing approvals organized in one location [1].

Broker-dealers have additional responsibilities under FINRA Rule 2210. This rule may require firms to file communications related to referral programs with FINRA’s Advertising Regulation Department to ensure they are fair, balanced, and not misleading [3]. FINRA is currently running a pilot program through December 31, 2025, allowing firms to upload revised communications without incurring extra filing fees [3].

| Requirement | Registered Investment Advisors (RIAs) | Broker-Dealers |

|---|---|---|

| Primary Regulation | SEC Marketing Rule (Rule 206[4]-1) [9] | FINRA Rule 2210 & Rule 3220 [3][1] |

| Written Agreement | Required for compensation >$1,000/year [1][9] | Required for certain non-cash arrangements [1] |

| Filing Requirement | Form ADV updates [9] | FINRA Advertising Regulation filings [3] |

| Recordkeeping | Rule 204-2 (Books and Records Rule) [9] | FINRA/SEC recordkeeping standards [3] |

Once you’ve established strong disclosure and documentation practices, it’s equally important to communicate referral arrangements clearly in client-facing materials. Use straightforward language that’s easy for the average person to understand. Make sure required documents - like your firm’s brochure (Form ADV Part 2A) - are provided at the time of the referral [4].

"Treat consent, disclosure, and documentation as strategic assets, not afterthoughts." – Select Advisors Institute [4]

To maintain consistency, use standardized disclosure templates [4]. This minimizes the risk of sending mixed messages about program terms, eligibility, or rewards across different platforms [1]. Whether clients are learning about your referral program through your website, social media, email, or a partner’s recommendation, the information should align.

When highlighting the benefits of your services, ensure a balanced presentation of risks and limitations, as required under the SEC Marketing Rule [9]. Avoid exaggerated claims or incomplete comparisons that could mislead clients about what your firm offers [1]. Your marketing materials should honestly reflect your services, costs, and any material restrictions.

It’s also important to regularly review all client acquisition channels - websites, social media accounts, and lead vendors - to confirm that disclosures are accurate and up to date [4]. Consider using compliance technology to pre-approve marketing materials before they’re published. This allows you to catch overly aggressive language or missing disclosures before they reach your audience [1].

Conflicts of interest occur when compensation or incentives influence recommendations in ways that might not align with a client’s best interests [12]. To identify these, take a close look at compensation structures - like revenue sharing, fees, commissions, bonuses, contests, and quotas - that could potentially create biases [12][13]. For example, if advisors earn more for recommending proprietary products or those tied to revenue-sharing agreements, they may prioritize the firm’s financial interests over the client’s.

Another red flag is when product recommendations are limited to a specific "menu" of options that financially benefit the firm. This restriction can reduce client choice and steer decisions away from what’s truly best for the client [12]. Regularly reviewing compensation models, especially after changes to business practices or product offerings, is essential [12]. If you’re working with influencer referrals, it’s equally important to conduct thorough background checks [5].

Once conflicts are identified, they need to be addressed promptly and effectively.

After spotting conflicts, there are three main ways to handle them: eliminate, mitigate, or disclose. The SEC emphasizes that disclosure alone isn’t enough - you must actively work to reduce the conflict’s influence [12][13].

Eliminate conflicts that can’t be managed properly. For instance, get rid of sales contests, quotas, or bonuses tied to selling specific securities within tight timeframes. If a conflict is too severe to address through other means, consider restricting certain professionals from recommending specific types of products [12].

For conflicts that can’t be entirely eliminated, focus on mitigation. One effective approach is to cap incentive thresholds and monitor recommendations closely. Avoid systems where advisors earn disproportionately higher pay for hitting certain sales targets, as these can encourage biased recommendations. Instead, standardize compensation across similar product lines, such as ensuring all mutual funds or annuities offer the same pay structure. If compensation varies, base those differences on neutral factors rather than the product’s profitability [12].

Set up supervisory monitoring systems to track recommendations that could lead to additional compensation. Pay close attention when advisors approach incentive thresholds or recommend higher-paying proprietary products. These safeguards align with broader compliance measures and reinforce a client-first approach.

"A conflict of interest is an interest that might incline a broker-dealer or investment adviser - consciously or unconsciously - to make a recommendation or render advice that is not disinterested."

– SEC Staff Bulletin [12]

Once conflicts are addressed, the focus shifts to protecting client interests. This requires a well-rounded approach built on four key principles: Disclosure (providing clear, detailed information), Care (ensuring recommendations are well-founded), Conflict of Interest (identifying and managing conflicts), and Compliance (enforcing policies through written guidelines) [12].

In addition to disclosure and recordkeeping requirements, you should maintain written supervisory procedures tailored to your referral programs. These should be updated regularly to reflect regulatory changes [5]. The procedures must clearly outline acceptable and unacceptable practices, provide guidance for evaluating investments in the client’s best interest, and specify consequences for failing to comply [12][5]. Regular audits of your materials, communications, and processes are also crucial to ensure alignment with both internal policies and federal standards [2].

Before bringing referral partners into your program, conduct thorough compliance and reputational checks. Review their past public activities and perform background checks to avoid potential risks [5].

When drafting disclosures, avoid vague or ambiguous language.

"An adviser disclosing that it 'may' have a conflict is not adequate disclosure when the conflict actually exists."

– SEC Division of Investment Management [13]

Be transparent about the specific nature of conflicts and detail how they’re being addressed. This ensures clients can make informed decisions with full awareness [12][13].

Lastly, promote a culture of compliance within your organization. Encourage financial professionals to identify and report conflicts without fear of repercussions [12]. Provide targeted training for both internal teams and external referrers on regulatory obligations and client protection standards [1][5]. Adjust compensation structures for individuals who fail to effectively manage conflicts [12]. By embedding these practices into your firm’s operations, you can prioritize client interests and maintain trust.

To create a compliant referral program, start by understanding the regulations that apply to your business model. Regulatory guidelines differ for broker-dealers, RIAs, and lenders, so it's essential to familiarize yourself with the specifics.

Transparency is key. Design incentive structures with clear, upfront disclosures about compensation and any potential conflicts of interest. Establish written supervisory procedures (WSPs) that clearly separate standard referral programs from those involving social media influencers. These procedures should be updated regularly to reflect evolving regulations [5]. Additionally, document every referral arrangement, including compensation details and disclosures, to support internal audits and regulatory examinations [1].

"When compliance and marketing teams collaborate early, they can design programs that align with business objectives and industry regulations, minimizing the risk of regulatory scrutiny."

– InnReg [1]

Finally, consider using the right tools and seeking expert guidance to ensure these principles are effectively implemented.

Compliance automation software can simplify the process by centralizing referral agreements, automating marketing approvals, and flagging issues like aggressive language or missing disclosures before materials are published [1]. Real-time monitoring tools can analyze referral patterns and identify unusual activity, such as fraud or self-referral schemes [1].

For specialized support, consulting services like Visora (https://visora.co) offer AI-powered business development systems and strategic consulting tailored to financial services leaders.

FINRA also provides valuable resources, such as the Advertising Regulation Electronic Files (AREF) system, which allows firms to submit communications for review to ensure they are fair, balanced, and not misleading [8]. Additionally, the Rulebook Search Tool (FIRST) can help firms identify specific requirements that apply to their activities [3][8].

A well-structured referral program can achieve both compliance and business growth. Referral leads often convert more effectively than cold prospects because they come with an established level of trust, reducing skepticism and cutting down on acquisition costs. This approach also strengthens client loyalty [1].

From the outset, align your growth objectives with regulatory requirements to ensure your program remains both effective and compliant [1]. Transparent disclosures about financial incentives not only build trust with potential clients but also improve the quality of leads. For RIAs operating under fiduciary duty, such transparency ensures that recommendations are based on merit rather than incentives, safeguarding both clients and the firm's reputation [1].

Financial referral programs come with a variety of compliance risks that businesses must address to steer clear of legal troubles or damage to their reputation. One major concern is adhering to industry regulations, such as those enforced by the SEC and FINRA. These agencies require firms to provide accurate disclosures and maintain oversight to ensure no misleading claims are made. Transparency is equally important, as the FTC requires companies to clearly disclose any financial incentives or material connections tied to referral arrangements.

Another area of concern is protecting customer privacy. Mishandling customer data or violating anti-spam laws can lead to serious consequences. On top of that, firms must comply with anti-bribery and anti-corruption laws, ensuring that any incentives offered are both appropriate and fully disclosed. Ignoring these regulations can result in steep fines, sanctions, or lasting reputational harm.

To avoid these pitfalls, financial firms should make regulatory compliance a top priority and establish strong compliance frameworks for their referral programs.

Financial firms can ensure openness in their referral program compensation by openly sharing details about financial incentives, relationships, or any potential conflicts of interest with their clients. This includes meeting the requirements of regulations like the SEC Marketing Rule (Rule 206(4)-1), which calls for clear disclosures about compensation arrangements and the nature of relationships with referrers.

It's equally important for firms to follow FTC guidelines, which emphasize the need to clearly communicate all material connections and incentives, steering clear of any practices that could mislead clients. Furthermore, firms must respect privacy laws and adhere to anti-spam regulations to protect client information and maintain trust. By focusing on clear communication and regulatory adherence, financial firms can strengthen their credibility and ensure their referral programs operate with integrity.

To steer clear of conflicts of interest in referral programs, financial firms should concentrate on three main areas:

Focusing on these areas helps financial firms uphold high ethical standards and create referral programs that clients can trust.

%20(5).png)