%20Bold.png)

Dynamic pricing is transforming financial services by replacing static rates with real-time, AI-driven adjustments. This approach personalizes prices based on customer behavior, market conditions, and risk profiles, delivering better profit margins and improved customer satisfaction. Key benefits include:

For example, Amplifi Capital increased loan acceptance rates by 30% in 2025 using dynamic pricing, while Equa Bank improved value for 70% of its clients with personalized rates. This shift is reshaping how financial products are priced, offering financial institutions a competitive edge.

In this article, learn how AI and predictive analytics power dynamic pricing across loans, deposits, insurance, and more, with actionable strategies for implementation.

Dynamic pricing is transforming the financial services landscape by delivering three key benefits: higher profit margins, improved customer satisfaction, and quick adaptability to market changes.

Traditional pricing often undervalues high-creditworthy clients, while dynamic models better capture their willingness to pay. These models also use algorithms to craft tailored offers for riskier profiles, balancing profitability with market expansion [1]. Instead of pricing products in isolated silos, financial institutions are shifting to a portfolio-level approach. This method optimizes Customer Lifetime Value (CLV) by considering a client’s entire range of products - like loans, deposits, and insurance - holistically [7]. For instance, Stripe's automated recovery tools helped users recover over $6.5 billion in revenue in 2024 [4]. Even a modest 1% price increase can lead to an 11.4% boost in operating profit for financial institutions [9]. These optimizations enable faster, more efficient customer interactions that directly impact the bottom line.

Customers today expect rewards that reflect their loyalty and relationship with financial institutions, yet many feel underserved in this area [8]. Dynamic pricing bridges this gap by offering real-time, personalized rewards. For example, a salary credit might immediately unlock better rates or upgraded account features [8]. This responsiveness fosters deeper customer satisfaction and loyalty.

Dynamic pricing also keeps financial firms competitive in a fast-moving market. Unlike static pricing models that require lengthy updates, dynamic systems allow real-time adjustments to market changes, protecting firms from falling behind competitors [1][8]. As Runa Mary Paul, Principal Architect at SunTec Business Solutions, explains:

"A sustainable model treats fairness, transparency, and customer value as non‑negotiable constraints, and uses dynamic tools to align price with value, not just to maximize yield" [8].

The financial rewards of dynamic pricing are hard to ignore. Companies implementing price optimization tools often see profitability gains between 5% and 19%, with dynamic pricing specifically boosting profits by 10% to 20% [9]. The global market for AI in ecommerce and financial pricing is expected to grow from $7.3 billion in 2024 to $64.0 billion by 2034 [4]. Firms that delay adopting these tools risk losing ground to competitors already reaping the benefits.

Instead of relying on static rate sheets, predictive analytics brings loan pricing into the modern age with dynamic, personalized offers. By analyzing real-time borrower data, market trends, and creditworthiness, machine learning models can predict how likely a customer is to accept a loan at various interest rates [10][3]. These models also pick up on behavioral cues - like the time of day a request is made, the device used, or whether the customer seems to be comparison shopping or in urgent need [1]. A great example of this in practice is Amplifi Capital, a UK fintech company. In 2024, they introduced a real-time dynamic pricing system for near-prime borrowers in the online broker market. The result? A 30% jump in offer acceptance rates, all while keeping profitability in check [1]. This kind of tailored pricing doesn’t just refine loan offers - it delivers measurable financial benefits.

AI-powered pricing strategies have proven to be a game changer for profit margins, increasing them by up to 15% through better risk segmentation and stronger customer retention [10]. For instance, a Boston Consulting Group case study highlighted a 26% rise in risk-adjusted returns when commercial loan pricing was optimized with AI [12]. Similarly, Equa Bank used AI to fine-tune pricing based on individual payment ability and behavioral patterns. This approach reduced application rejections caused by mismatched, generic offers, benefiting about 70% of their clients [1]. As McKinsey & Company puts it:

"Institutions that adopt dynamic pricing strategies have seen profit margins increase by up to 15% due to better risk segmentation and improved customer retention" [10].

Dynamic pricing isn’t just about boosting the bottom line - it’s also about fairness and transparency. By tailoring rates to individual risk profiles instead of lumping borrowers into generic categories, banks can offer more equitable loan terms [3]. Borrowers benefit from offers that reflect their unique financial behaviors, credit histories, and even their relationship with the institution [10][7]. And with 59% of banking customers saying they’d switch banks for better interest rates, personalized pricing is quickly becoming a must-have for retaining customers [12].

Reinforcement Learning (RL) takes dynamic pricing to the next level. It allows banks to continuously improve their strategies by rewarding positive outcomes - like higher conversions and profitability - while adjusting for risks like defaults [3]. Unlike static A/B testing, RL evolves in real time, adapting to changes in customer behavior and market conditions [3]. Soumyadeep Maiti, Director of Data Science at Tredence, explains it best:

"Reinforcement learning (RL) is a transformative approach that allows banks to learn and adapt their loan pricing strategies in real time" [3].

To balance compliance with innovation, hybrid systems combine rule-based engines for regulatory requirements with machine learning to spot patterns in customer behavior [11]. Banks can also test these advanced models with pilot programs - say, for small business loans - before going all in [12]. This ongoing refinement helps banks stay competitive by ensuring their pricing strategies keep up with market trends and customer expectations.

Banks are moving away from static deposit rates, embracing real-time pricing that adapts to market conditions. Using machine learning, these systems analyze behavioral signals - like balance patterns, potential churn, and sensitivity to pricing - to determine the best rate for each customer at any moment. For example, they can identify "life events", such as unusually large deposits, and offer tailored rates before those funds are transferred to a competitor. These decisions are made in milliseconds, ensuring timely action [1][13][14]. Devon Kinkead, Founder and CEO of Micronotes, highlights the importance of speed in this process:

"Generative AI can now push deposit-pricing recommendations to decision-makers in hours instead of weeks. That speed wins deposits at a lower cost of funds - if you can turn the model's output into timely, personal conversations" [13].

This rapid, data-driven approach not only improves responsiveness but also sets the stage for meaningful financial gains.

Dynamic pricing strategies have demonstrated a measurable impact on revenue. Optimized deposit pricing can yield an uplift of 8 to 18 basis points [14]. A notable example is a US bank that, in July 2025, reduced annual interest expenses by $45 million on a $140 billion deposit portfolio by implementing segmented pricing strategies. These strategies focused on customer behavior and value potential, targeting incentives to retain and attract customers rather than overpaying rate-sensitive individuals who frequently switch banks for higher yields [14].

One effective tactic is offering bonus interest for balances maintained consistently over six months, encouraging deposit stability. This not only enhances funding duration but also strengthens the overall quality of the balance sheet [14].

Much like dynamic loan pricing, real-time deposit rate adjustments prioritize fairness and personalization. Instead of relying on broad, tiered products, banks can offer rates tailored to each customer’s relationship with the institution and their deposit behavior [14]. Behavioral segmentation helps identify customers likely to leave or explore competitors, enabling proactive rate offers to retain them [14].

AI-driven models have proven effective in increasing customer engagement by leveraging behavioral insights. The shift from basic demographic segmentation to hyper-personalization allows banks to better understand individual needs through tools like "micro-interviews" and digital behavior tracking [13]. This evolution ensures that customers feel valued and receive rates that reflect their unique circumstances.

Modern deposit pricing systems are designed for speed and flexibility. Centralized pricing engines separate pricing logic from core systems, allowing business teams to adjust rules without requiring complex coding. This reduces implementation times from months to weeks [15]. Reinforcement learning algorithms continuously refine pricing strategies, optimizing for long-term goals like Net Present Value [3].

Generative AI further accelerates the pricing cycle, shrinking it from weeks to hours and producing ready-to-use materials for decision-makers [13]. The true advantage lies in pairing this intelligence with an "action layer" that delivers personalized offers directly to customers via mobile apps, SMS, or email. These systems ensure that offers are sent the moment a relevant market signal is detected [13]. A smart way to begin is by piloting the strategy with high-impact segments, such as near-maturity CDs over $50,000, to assess results before scaling up [13].

Reinforcement learning (RL) takes a different approach to loan pricing compared to traditional methods. Instead of relying solely on static rules or historical data, RL employs an autonomous agent that interacts with the market environment to learn and refine optimal pricing strategies over time [16][17]. This agent adjusts loan rates dynamically to maximize cumulative revenue or profit [19].

What sets RL apart is its ability to respond to sudden market changes by learning continuously from real-time feedback, rather than waiting for manual updates [17][19]. For simpler scenarios, Q-Learning models are effective, while more complex datasets often require Deep Q-Networks (DQN) [18][19]. Tomas Heiskanen and Barton Friedland from Thoughtworks highlight this advantage:

"Online reinforcement learning is different in that it can rapidly adapt to ever changing price elasticity through rapid and real-time automated price experimentation, avoiding reliance on historical data" [17].

This adaptability not only improves pricing strategies but also drives better revenue outcomes.

Case studies from companies like Amplifi Capital and Equa Bank show how RL implementation can lead to measurable gains. For example, these firms reported a 30% increase in loan acceptance rates along with notable improvements in margin optimization across the industry [1][5][22]. Broader data supports these findings, with AI-driven predictive pricing delivering a 25% boost in margin optimization and revenue growth ranging between 5% and 25% [5]. RL models excel at capturing higher margins during peak demand periods while simultaneously preventing revenue losses by adjusting prices in real time to align with inventory and market trends [5][22].

RL enables banks to move away from generic pricing models toward personalized rates that reflect each customer's unique and evolving profile. Instead of relying solely on static factors like credit scores and income, RL evaluates a customer’s entire portfolio and wallet share to determine a tailored "relationship price" [21]. This system also incorporates real-time behavioral data - such as app usage patterns, timing of requests, and device preferences - to understand where customers are in their decision-making process, whether they’re exploring options, in urgent need, or undecided [1].

Ghela Boskovich, Regional Director at the Financial Data and Technology Association, explains this shift:

"A shift to a dynamic pricing strategy means no longer looking at individual products as revenue drivers, but at the individual customer's portfolio of products and services as the revenue driver" [21].

This approach allows banks to bundle products with varying profitability levels, offering discounts on price-sensitive items while maintaining overall portfolio profitability. By continuously adapting to customer behavior, RL enhances the integration of AI across multiple financial products.

RL models are designed to balance exploration - testing new pricing strategies to gauge market elasticity - and exploitation, which involves leveraging already proven profitable price points [16][18]. This continuous refinement focuses on long-term goals like Net Present Value, rather than short-term revenue spikes [16][19].

To implement RL effectively, banks are encouraged to start small, piloting the technology on a specific product or customer segment before scaling up [17][20]. Transparency is key - clearly explaining the rationale behind AI-driven pricing adjustments helps build customer trust and ensures compliance with fair lending regulations [10][20]. Additionally, internal alignment is crucial; sales teams must be incentivized to follow AI-recommended pricing strategies, as manual overrides can disrupt the model’s learning process [20].

Price sensitivity models, often called "propensity to buy" models, rely on machine learning to predict how likely a customer is to accept an offer at various price points [1]. These models assess price elasticity, which gauges how demand for loans or credit products shifts when interest rates or fees are adjusted [9].

These tools can identify where a customer is in their decision-making process. By analyzing AI signals and real-time behavioral data, they can determine if someone is casually browsing, urgently seeking options, or hesitating on a decision [1]. Automated systems then adjust pricing dynamically on mobile apps and web platforms [1].

Financial institutions are also leveraging micro-segmentation to develop highly detailed customer profiles. These profiles consider factors like lifestyle, purchase patterns, and urgency, enabling pricing strategies tailored to individual needs rather than broad demographic categories [9]. For instance, high-risk customers often show less sensitivity to price changes because their limited credit options make approval more valuable than a lower rate [9].

As with other dynamic pricing tools, these models align pricing strategies with customer value and behavior.

The precision of these models not only fine-tunes pricing strategies but also significantly boosts revenue. For example, a mere 1% improvement in price realization can lead to an 11.4% increase in operating profit [9]. Companies that implement price optimization tools typically see profitability gains ranging from 5% to 19%, with dynamic pricing models contributing 10% to 20% increases in profits [9][4].

Equa Bank provides a compelling example. By using a pricing model that tailored interest rates to individual payment capacities and behaviors, the bank enhanced value for 70% of its clients while reducing application rejections [1].

These models represent a shift from a product-focused to a customer-focused pricing strategy. Instead of treating individual products as isolated revenue sources, banks now evaluate a customer's entire portfolio of products and services [21]. Dominik Matula, Head of AI, Data Science & Machine Learning at Profinit, highlights this approach:

"It's a data-driven model that uses artificial intelligence to deliver the most appropriate price to each customer, so that it is fair for the individual and profitable for the provider" [1].

This "relationship pricing" strategy considers a customer's overall value, including wallet share, loyalty, and transaction history. By offering personalized rates that reflect the customer's unique relationship with the institution, banks can improve acceptance rates and foster long-term loyalty. It’s not just about the price - it’s about delivering offers that align with the customer’s needs in terms of timing and format, ultimately building trust [1].

As these personalized models are refined during pilot programs, they become scalable for wider application.

Testing these models on a single product line with clear price boundaries - such as floors and ceilings - helps quickly identify and address margin leaks while maintaining regulatory compliance [4][9][23].

It’s also crucial to monitor how elasticity changes over time. For example, a borrower’s sensitivity might start at -1.1 in the first year but increase to -2.9 by the third year as they explore alternative options [9]. To fine-tune pricing strategies, targeted research methods like surveys or conjoint analysis can help define optimal pricing thresholds [23].

Financial institutions have long applied AI to optimize pricing for loans and deposits. Now, similar methods are transforming foreign exchange (FX) transactions, offering a chance to stay ahead in a fast-moving market.

The FX market moves at lightning speed - sometimes changing in milliseconds. AI-powered systems can now process massive amounts of data, including competitor price updates, macroeconomic trends, and market volatility, to adjust prices instantly. These systems use machine learning to spot patterns in both historical and live data, such as demand spikes triggered by major news or economic shifts, and adapt prices accordingly. Reinforcement learning further helps refine pricing strategies by testing adjustments in real time, measuring results like revenue growth or conversion rates. Additionally, propensity-to-buy models predict how likely customers are to accept specific FX rates, while automated safeguards like price floors and ceilings ensure stability even during extreme market shifts [1][4].

Gone are the days of static PDF price lists. Automating FX pricing with real-time algorithms allows firms to capture higher margins for every quote. On average, companies using AI-driven dynamic pricing report revenue increases of 15% to 25% [26]. Leaders in revenue growth often implement these strategies twice as often as competitors, achieving win rates 12 percentage points higher [25]. As Stripe puts it:

"The result is a pricing system that adapts to reality rather than assumes that yesterday's price is still the right one today" [4].

AI-driven dynamic pricing also offers a personalized touch by analyzing where a customer is in their buying journey - whether they’re casually browsing, urgently comparing options, or hesitating before committing. By understanding individual behavior and price sensitivity, firms can adjust FX rates to reflect perceived value. This approach not only improves customer satisfaction and loyalty but also builds trust. Customers are more likely to see price changes as fair when they understand they’re tied to factors like market demand or volatility [1][22]. By delivering tailored pricing, businesses strike a balance between profitability and fairness.

Scaling dynamic FX pricing starts with clean, well-organized data from sources like competitor feeds, market indices, and past transactions. Running A/B tests can help compare dynamic models against static ones to identify revenue improvements. With a capable technical partner, implementing a dynamic pricing platform typically takes 4 to 8 weeks. Annual costs range from $50,000 to over $500,000, depending on company size and complexity [25][26]. Weekly reviews of pricing accuracy and system performance ensure the model adapts to evolving market conditions. Additionally, strict rate-of-change limits prevent erratic pricing, maintaining customer trust [4].

AI-driven discount strategies are a key part of any dynamic pricing approach, ensuring that offers remain both competitive and profitable. While discounts can help close deals, they often erode profitability when used indiscriminately. Research reveals that over 40% of discount requests in banking lack justification based on objective client characteristics [6]. This misalignment leads to significant revenue leakage, with some industries experiencing discount rates that exceed 50% of the headline prices [6].

AI tools leverage historical win/loss data from thousands of transactions to determine the optimal discount required to close a deal. By evaluating price elasticity and a customer's "propensity to buy", these systems can pinpoint which clients are likely to pay higher rates and which genuinely need a discount to convert [2][6][1]. Machine learning also identifies "at-risk" customers - those who may need incentives to renew - while flagging loyal clients with high usage who don’t require extra discounts. As Simon-Kucher partner Silvio Struebi explains:

"AI-powered decision support tools can help structure discount practices at point of sale, improving overall pricing consistency and reducing the risk of unfair treatment." [6]

This precise approach ensures discounts are applied strategically, minimizing revenue loss while boosting profitability.

AI models provide real-time recommendations for "Walk-Away" and "Target" prices, reducing reliance on gut instincts [2][24]. Automated systems catch inconsistencies in discounting and align offers with broader strategic objectives. The benefits are clear: digitized discount workflows can cut manual pricing approval times by 50% to 60% [6]. Financial institutions that have embraced AI-driven discount optimization report higher offer acceptance rates without sacrificing profitability [1].

These AI-driven discount methods do more than just protect revenue - they also align pricing with each customer's specific value. By quantifying the "Value in Use" for individual clients, AI enables personalized pricing that reflects actual customer circumstances while safeguarding profit margins [2][6]. This approach goes beyond broad customer categories, creating thousands of finely-tuned profiles based on real-time data signals. Unlike arbitrary negotiation tactics, this strategy delivers pricing that feels fair because it’s tailored to each client’s unique needs.

Centralizing pricing functions in a "Center of Excellence" eliminates fragmented strategies and ensures consistency [24][6]. Embedding AI-driven pricing recommendations directly into CRM systems gives relationship managers the confidence to negotiate using data-backed insights, while automated governance tools enforce compliance in real time [24]. Adjusting performance metrics to prioritize profitability and margin preservation over sheer volume growth further aligns incentives [6]. As ChatFin succinctly puts it:

"The 'Price List' PDF is a relic. The price is whatever the algorithm says it is, at this precise second, for this specific customer." [2]

Credit card pricing has evolved to combine real-time behavioral insights with traditional risk metrics. Machine learning models now analyze factors like request timing, device type, and browsing habits to gauge whether a customer is acting urgently or hesitantly [1]. These "propensity-to-buy" models estimate how likely someone is to accept a specific offer [1]. On top of that, prescriptive analytics helps balance revenue goals with regulatory requirements and credit risk limits [27].

Using Reinforcement Learning, banks continuously adjust pricing based on real-time customer interactions. This allows them to target "near-prime" customers - those who might not qualify under traditional models but could be approved with a better, risk-adjusted offer [1]. Dominik Matula, Head of AI, Data Science & Machine Learning at Profinit, explains:

"Creditworthy clients may accept slightly higher prices, while riskier clients can be offered lower ones, while still within acceptable risk levels" [1].

Much like dynamic pricing in loans and deposits, these models combine real-time behavioral and risk data to deliver tailored offers. This approach not only personalizes pricing but also opens up opportunities for increased revenue.

Česká Spořitelna’s use of FICO Pricing Optimization is a prime example of this strategy in action. The bank saw new sales jump by 29%, while average profit per account grew by 26%, all without increasing credit risk costs [27]. Zuzana Sloukova from the bank’s Retail Risk department shared:

"When the strategy went live, it outperformed our expectations. APP increased 26%, and new sales increased 29%, without an increase in credit risk costs" [27].

By tailoring pricing to customer payment capacity and behavior, AI-driven models have brought measurable value to nearly 70% of a bank’s client base [1].

Dynamic pricing principles allow risk-based models to go a step further, creating highly personalized offers. This is especially important when nearly 59% of banking customers are willing to switch providers for better rates [12]. By analyzing payment habits, browsing behavior, and sensitivity to discounts, AI enables banks to build detailed customer profiles that reflect both risk and potential value [4].

Equa Bank embraced this approach by optimizing its pricing model around customers' payment behavior and financial capacity. The result? Increased revenue and fewer application rejections caused by mismatched, overpriced offers. Around 70% of their clients benefited from this tailored strategy [1]. This precision ensures competitive rates for high-creditworthy customers while offering feasible options to riskier segments, avoiding unnecessary rejections.

To build effective risk-based pricing systems, banks must establish clear price floors and ceilings to ensure rates remain aligned with brand standards and regulatory requirements [4]. Starting with small-scale pilot programs allows institutions to measure performance and identify any unintended consequences before expanding [4].

Integrating multiple data streams - such as historical transactions, real-time behavioral signals, and competitor pricing - ensures that pricing decisions are both accurate and up-to-date [4]. Additionally, embedding compliance rules directly into machine learning models guarantees that automated pricing meets regulatory and fairness standards [3].

This scalable, data-driven approach transforms pricing from a reactive process into a proactive strategy. Banks that have adopted advanced analytics for loan pricing have reported profitability increases of 10% to 20%. Meanwhile, AI models designed for commercial loan pricing have delivered an average 26% boost in risk-adjusted returns [12].

The insurance industry is moving beyond traditional, static actuarial models that rely heavily on historical data and broad demographic assumptions. Thanks to advancements in technology, tools like telematics, wearables, and IoT sensors now provide real-time insights. For example, auto insurers can track driving habits, health insurers can monitor physical activity, and home insurers can assess environmental risks in real time.

Incorporating external data sources further sharpens this approach. Real-time updates on weather conditions, local crime statistics, and competitor pricing feed into predictive models, allowing insurers to adjust premiums dynamically based on current risks rather than relying on outdated averages. Every interaction - whether a quote is accepted or rejected - serves as valuable feedback, helping self-learning algorithms refine their predictions over time. This integration of real-time data is paving the way for more precise, risk-based premium adjustments.

Dynamic pricing has proven to be a game-changer for insurers aiming to optimize revenue. For instance, GEICO reported a significant jump in underwriting earnings, from $703 million in Q1 2023 to $1.928 billion in Q1 2024, by leveraging advanced data analytics for more accurate risk assessments [28]. AI-driven pricing models are capable of aligning premiums within 2%–3% of a customer's actual risk profile, which can lead to profit margin increases of 10%–15% [28][29].

Similarly, Amplifi Capital, a fintech company in the UK, saw a 30% rise in offer acceptance rates after adopting real-time dynamic pricing through a cloud-based system [1]. In another example, Findevor identified a $60 million projected incremental written premium opportunity on a $1 billion portfolio by using distribution intelligence [30]. Alex Valdes, Founder and CEO of Findevor, emphasized:

"Distribution decisions materially shape portfolio outcomes, yet they are often managed through fragmented reporting and intuition. By integrating distribution into portfolio management, we turn performance insight into immediate, forward-looking action" [30].

These examples highlight how aligning premiums with real-time risk assessments can drive both revenue growth and operational efficiency.

For dynamic pricing to succeed, customers need to see a clear connection between their behavior and their premiums. Instead of employing surge pricing, which can feel punitive, insurers often use dynamic discounting. This approach sets a standard price but offers discounts for low-risk behaviors, such as safe driving or healthy habits.

This transparency builds trust. Studies have shown that personalized pricing models can improve customer satisfaction and retention rates by 20%–30%. A notable example is Root, an American auto insurer that uses IoT technology to monitor driving behavior. Safer drivers are rewarded with lower premiums, making the insurance experience more tailored and fair [28][29]. This shift turns insurance from a generic product into a personalized service that better reflects individual risk profiles.

Implementing dynamic pricing at scale requires a robust data infrastructure. Insurers must integrate internal systems like CRM platforms with external data sources, such as weather feeds, market trends, and IoT devices [28]. To ensure fairness and compliance, price floors and ceilings must be established to keep premiums within acceptable ranges and regulatory guidelines [22]. Automated processes should also anonymize personal data to protect privacy while still enabling effective behavioral analysis [28].

Starting with pilot programs targeting specific customer segments is a practical way to test and refine dynamic pricing strategies. Cloud-based platforms make it possible to adjust premiums in real time, responding to changes like competitor pricing or external events within milliseconds [29]. This adaptability ensures that dynamic pricing remains a sustainable and evolving strategy across the financial services landscape.

Generative AI brings a fresh approach to pricing by continuously updating models based on real-time market prices and macroeconomic indicators, eliminating the need for periodic manual updates [33]. This technology also taps into previously untapped data sources, like sales call transcripts and customer sentiment analysis, giving pricing teams a broader perspective [31].

Large language models (LLMs) combine forecasting, causal reasoning, and business rules into an automated workflow, making pricing decisions more nuanced and context-sensitive. Instead of relying on static assumptions, these models adapt dynamically to customer signals, improving pricing strategies [33]. Financial institutions, for instance, can run continuous A/B tests on smaller market segments to assess price elasticity. This helps them find the "efficient frontier" for revenue growth without jeopardizing their entire customer base [2].

The impact of generative AI on revenue is clear, with case studies showing substantial growth. Companies in the top quartile of performance are twice as likely to use AI in sales and marketing compared to their lower-performing peers [31]. Sales teams leveraging data-driven insights report winning more deals than they lose, with a 12-percentage-point advantage over competitors [31]. Roman Kleinerman, VP of Products at Noodoe, an EV charging operator, shared:

"We've seen revenue increases of 10–25% depending on the location and number of stations" [33].

Bain & Company highlights the broader implications of this shift:

"The shift toward AI-enhanced pricing isn't just an upgrade to existing systems but rather a fundamental rethinking of this most basic business activity" [31].

By testing pricing strategies in virtual environments before rolling them out live, companies can minimize risks while maximizing profit margins [31][32].

Beyond revenue growth, generative AI makes advanced pricing capabilities more accessible across organizations. It lowers technical hurdles, enabling smaller firms to use sophisticated pricing tools through simple natural language prompts instead of requiring custom code or large data science teams [34].

To ensure compliance and control, companies should establish pricing guardrails - automated safeguards that prevent AI-driven pricing changes from violating fair lending laws or exceeding customer-facing limits. These guardrails balance the agility of dynamic pricing with the need for oversight [2][33]. Starting with a minimum viable product (MVP) for a small subset of products allows teams to fine-tune the model before scaling up [31]. Continuous retraining, whether daily or weekly, keeps models aligned with market trends, while manual overrides ensure human oversight in sensitive areas [33].

Offer optimization algorithms take dynamic pricing a step further by tailoring customer-specific offers to maximize long-term value.

This strategy follows a clear three-step process: first, it assesses the customer’s context - factors like their decision-making stage, timing, and the device they’re using. Next, it models their price sensitivity, estimating how likely they are to accept offers at different price points. Finally, it aligns these insights with goals that focus on maximizing Net Present Value (NPV) [1].

Reinforcement Learning (RL) plays a key role in fine-tuning these pricing decisions. As market conditions and customer behaviors shift, RL adapts in real time, moving away from traditional cost-plus pricing to a value-based model. This approach factors in efficiency improvements and risk reduction tailored to each client [3][2]. The result? A more personalized and financially rewarding strategy.

Take Amplifi Capital, a fintech company in the UK. By implementing real-time dynamic pricing for near-prime lending, they saw a 30% increase in offer acceptance rates, all while maintaining profitability [1]. This example highlights how financial institutions can move from static pricing to agile, value-focused strategies across their product offerings.

Scaling these algorithms requires robust analytics and cloud-based automation to handle real-time data and rapidly deploy models [27][1]. Dominik Matula, Head of AI, Data Science & Machine Learning at Profinit, shared:

"The system operates automatically, requires no manual input, and self-adjusts to market developments through continuous learning" [1].

To ensure success, businesses often start small, testing algorithms on limited customer segments in pilot programs. These trials, which typically last a few weeks to months, provide valuable insights before a full-scale rollout [1]. Continuous A/B testing on smaller market segments allows companies to measure price elasticity and refine their models without risking their broader customer base [2].

However, it’s crucial to establish pricing guardrails. These safeguards help companies avoid violating fair lending laws or antitrust regulations while maintaining transparency in their pricing strategies [2].

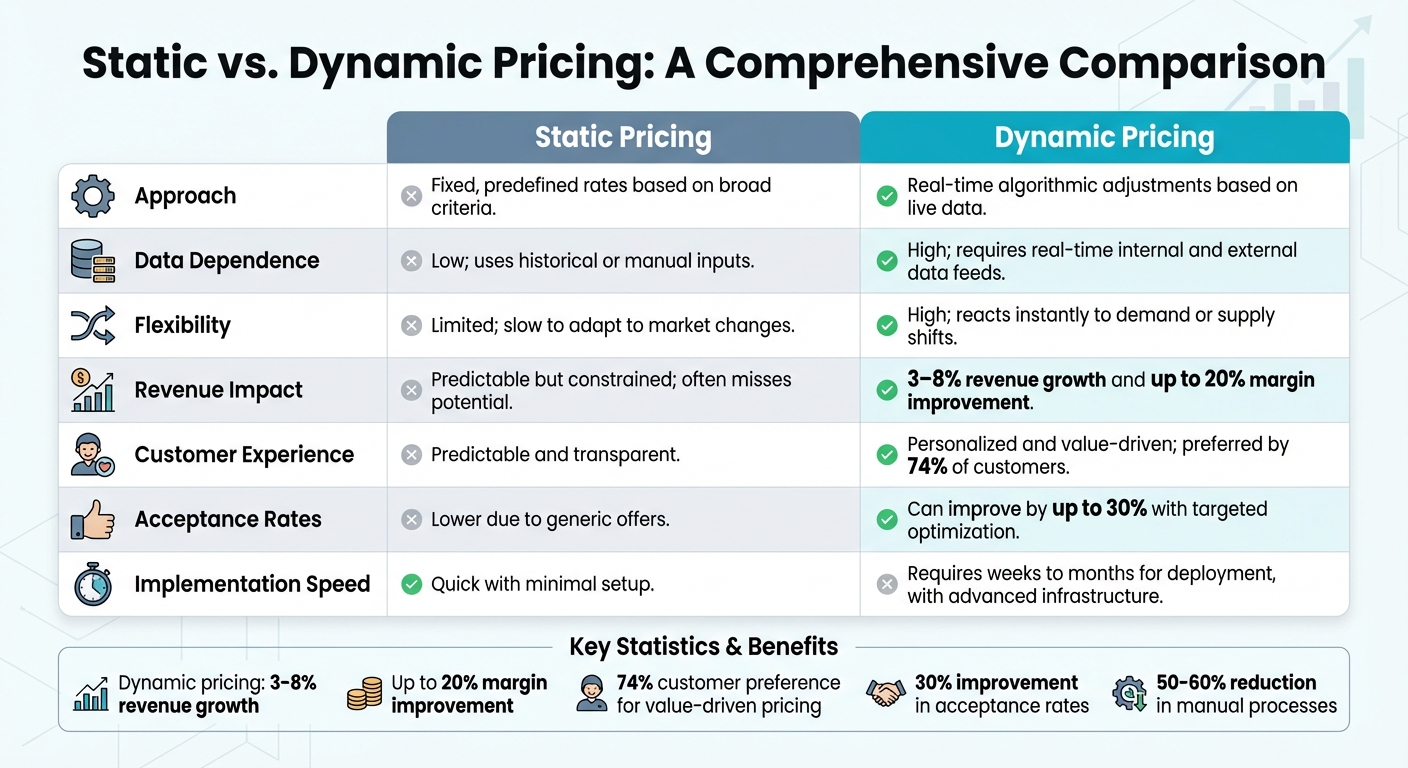

Static vs Dynamic Pricing in Financial Services: Key Differences and Impact

To summarize the differences, here's a table that highlights how static and dynamic pricing approaches vary across several key factors.

Static pricing relies on fixed rates and broad customer categories, making it straightforward but slow to adapt to market changes. On the other hand, dynamic pricing adjusts prices in real time, leveraging algorithms and machine learning to respond to demand, competition, and individual customer behavior [35][1]. While static pricing is easier to manage, it often misses opportunities to maximize revenue. Dynamic pricing, however, can significantly boost profitability - companies using these systems report revenue increases of 3–8% and margin gains of up to 20% [35]. In financial services, dynamic pricing has driven profit margin growth of up to 15% [10].

Customer experience is another area where these approaches diverge. Static pricing provides a predictable but rigid experience, treating all customers the same. Dynamic pricing, by contrast, tailors offers to individual contexts, creating a more personalized experience. Notably, 74% of customers prefer pricing models that reflect the value they receive [36].

Implementation is also a major consideration. Static pricing is quick to set up and doesn't require much infrastructure. Dynamic pricing, however, involves a more complex rollout, needing robust data pipelines, real-time APIs, and constant model updates, which can take weeks or even months to implement [35][4].

| Factor | Static Pricing | Dynamic Pricing |

|---|---|---|

| Approach | Fixed, predefined rates based on broad criteria | Real-time algorithmic adjustments based on live data |

| Data Dependence | Low; uses historical or manual inputs | High; requires real-time internal and external data feeds |

| Flexibility | Limited; slow to adapt to market changes | High; reacts instantly to demand or supply shifts |

| Revenue Impact | Predictable but constrained; often misses potential | 3–8% revenue growth and up to 20% margin improvement [35] |

| Customer Experience | Predictable and transparent | Personalized and value-driven; preferred by 74% of customers [36] |

| Acceptance Rates | Lower due to generic offers | Can improve by up to 30% with targeted optimization [1] |

| Implementation Speed | Quick with minimal setup | Requires weeks to months for deployment, with advanced infrastructure [35][4] |

This comparison highlights why dynamic pricing stands out as a more effective strategy, especially in industries where personalization and agility are key to success.

AI-powered dynamic pricing is transforming financial services by replacing outdated static rate lists with real-time, algorithm-based pricing that delivers measurable outcomes. For example, implementations in the field have significantly increased offer acceptance rates[1]. This shift is redefining how banks, lenders, and wealth managers capture and deliver value.

In addition to improving sales performance, automated discount workflows can reduce manual processes by 50–60%, allowing relationship managers to move away from time-consuming spreadsheet negotiations. Instead, they can rely on AI-driven tools for data-backed pricing recommendations[6][24]. These systems also reveal that over 40% of discount requests lack objective justification based on client data[6]. This not only minimizes revenue loss but also ensures customers receive tailored offers that align with their specific risk profiles. Industry experts emphasize this operational improvement.

Silvio Struebi and Alan Lim from Simon-Kucher highlight:

"AI-based pricing is not just about automation; it is about creating a smarter, more strategic approach to pricing that reflects market realities, client needs, and regulatory requirements"[24].

Case studies from Amplifi Capital and Equa Bank demonstrate the real-world impact of dynamic pricing, showing how it drives meaningful results. The real question isn’t whether dynamic pricing will become the norm in financial services - it’s whether your organization will take the lead or struggle to keep up. These strategies build on the principles of personalization and risk adjustment discussed earlier. To get started, consider establishing a Pricing Center of Excellence, aligning sales goals with profitability targets, and piloting AI models within a specific segment to gain an edge.

For financial services leaders in the U.S. looking to take the lead, Visora provides tailored AI-driven growth solutions to help implement these dynamic pricing strategies effectively.

Dynamic pricing in the U.S. financial services sector is generally allowed, provided it relies on objective factors like supply, demand, or seasonal trends. However, regulations are shifting to prioritize transparency and fairness. In some states, businesses must disclose the algorithms behind their pricing strategies.

Legal issues can emerge if sensitive consumer data is misused, potentially breaching privacy laws. To avoid these risks, companies should work closely with legal experts and ensure their pricing practices are clearly communicated to customers. This approach helps maintain compliance and builds trust.

To make dynamic pricing work, you’ll need access to a variety of data, like transaction histories, customer profiles, market trends, competitor pricing, and customer behavior. AI-powered tools take all this information from different sources and use it to guide pricing strategies.

Two major elements play a big role here: keeping an eye on competitor prices and monitoring changes in demand. By analyzing these factors, businesses can fine-tune their pricing to maximize revenue, update prices in real time, and even create personalized offers tailored to individual customer preferences.

Firms can build trust and transparency in AI-driven pricing by openly explaining how prices are set. This includes detailing the data sources used and factors such as market trends or customer behavior that influence pricing decisions. Establishing strong governance is also key to ensuring algorithms remain impartial and free from bias. Regular testing and monitoring can help spot and address any unfair patterns that may arise. Additionally, offering customers clear explanations about pricing decisions and accessible dispute resolution options strengthens trust and encourages lasting relationships.

%20(5).png)