%20Bold.png)

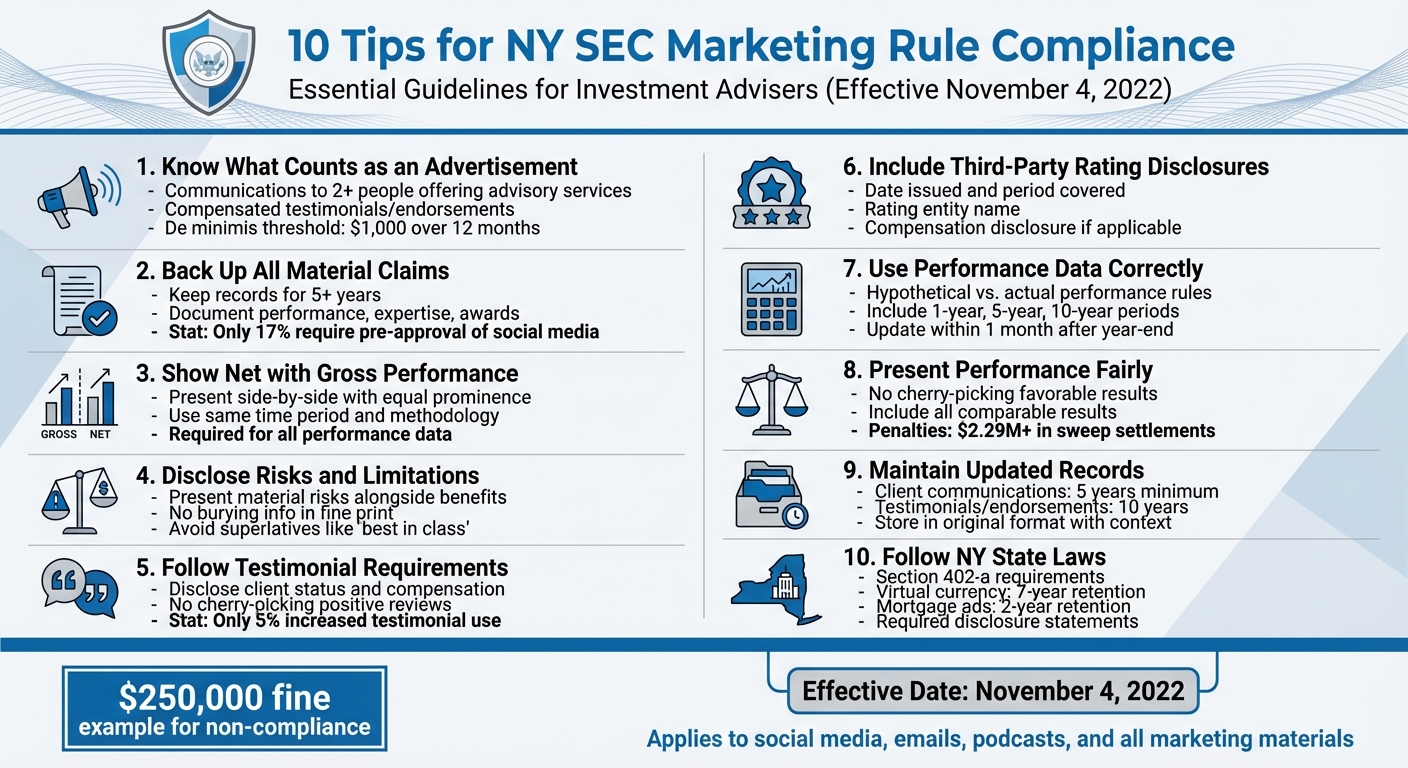

The SEC's Marketing Rule, effective November 4, 2022, has reshaped how investment advisers communicate, covering everything from social media posts to client emails. Compliance is mandatory to avoid penalties and reputational harm, especially for firms in New York, which face additional state-level regulations. Here's what you need to know:

Key takeaway: Compliance requires thorough documentation, clear disclosures, and careful oversight of all marketing materials. Failing to meet these standards can lead to fines, license issues, and damaged trust. Stay ahead by ensuring your firm's practices align with both federal and state regulations.

10 Essential SEC Marketing Rule Compliance Tips for NY Investment Advisers

The SEC categorizes advertisements in two main ways:

One area that often causes confusion is one-on-one communications. While these are typically excluded, they can be classified as advertisements if they involve hypothetical performance or any form of compensation. For instance, if a one-on-one email discusses projected returns, it falls under SEC regulation. Similarly, indirect communications - like relying on third-party content - are also treated as advertisements. This distinction between direct and indirect communication underscores the need for strong oversight of all messaging.

The SEC also defines "de minimis compensation" as $1,000 or less (or its non-cash equivalent) over a 12-month period [5]. If compensation exceeds $1,000 within that timeframe, it triggers Prong 2 of the rule. It’s worth noting that while live oral communications are excluded, recordings of those conversations are not [9].

To stay compliant, take these steps:

When it comes to advertising, you can only make claims you can prove. Isaac Mamaysky, Partner at Potomac Law Group, explains this clearly: any statement about performance, expertise, or service benefits in your marketing must be backed by solid documentation that you can provide if asked [1]. This rule is the foundation of honest and compliant advertising.

The SEC puts it plainly:

"If an adviser is unable to substantiate the material claims of fact made in an advertisement when the Commission demands it, we will presume that the adviser did not have a reasonable basis for its belief" [1].

Failing to follow this principle can be costly. One RIA faced a $250,000 fine for paying social media influencers without proper disclosures or documentation [13].

To stay compliant, make sure you document all types of claims:

Recordkeeping is not optional. The SEC requires you to store all written communications with clients, such as emails and newsletters, for at least five years [13]. This practice protects you during an SEC review. However, only 17% of compliance professionals currently require employee social media activity to be pre-approved, even though posts are subject to SEC marketing laws [13]. That leaves a major compliance gap.

To protect your firm, store all drafts, final versions, and supporting documents in a centralized, easily accessible system [12]. Also, maintain a clear audit trail for your marketing process, including due diligence for awards or rankings participation [12]. If you make judgment-based decisions - like using model fees instead of actual fees - document your reasoning and the supporting facts. This documentation will be your strongest defense during an SEC examination [15].

When showcasing performance data in marketing materials, you must include both gross and net performance. The SEC mandates that these figures be presented side by side, with equal prominence [11][17]. This ensures that clients see the full picture - what the investment earned before fees and what they actually received after costs.

The SEC has clear rules about how these numbers should be calculated and displayed. Both net and gross performance must use the same time period, return type, and methodology [11]. For instance, if Gross IRR excludes the impact of a subscription facility, Net IRR must exclude it as well. Any inconsistency in methodology violates the requirements [11]. These rules also apply to extracted performance data.

"The rule requires that any presentation of gross performance be accompanied by a presentation of net performance that has been calculated over the same time period and using the same type of return and methodology as the gross performance." - SEC Division of Investment Management [11]

The SEC has also provided specific guidance for unique cases. On March 19, 2025, it issued updates allowing for some flexibility with "extracted performance", which refers to results from a specific subset of investments. In such cases, gross performance for the subset can only be shown separately if the overall portfolio's gross and net metrics are presented immediately beforehand [16][17][18].

Additionally, if future fees are expected to exceed historical rates, you must use a model fee to reflect the higher costs. Failing to do so could result in a misleading net performance presentation [11].

When it comes to transparency, balanced risk disclosures are just as important as accurate data and performance claims. The SEC Marketing Rule emphasizes the need to present material risks alongside potential benefits[19]. This means you can't highlight the positives of your services while downplaying what could go wrong. This approach ties directly to anti-fraud protections, ensuring investors have the full picture before making decisions.

For example, if you're showcasing a case study of a profitable investment, you must also disclose the overall performance of the related strategy or fund during the same timeframe[19]. Highlighting a successful real estate deal? Then include context about how other similar investments performed. As Troutman Pepper explains:

"It would not be fair and balanced for an RIA to present case studies only reflecting profitable investments when there are similar unprofitable investments"[19].

Your disclosures should be clear and easy to find - no burying critical information in fine print or dressing it up with marketing language[10][14]. If you're using hypothetical performance data, you must provide additional details to help your audience understand the risks of relying on projections instead of actual results[4]. This aligns with the earlier focus on rigorous documentation and performance standards.

Failing to comply with these requirements can have serious consequences. If the SEC requests evidence to back up your claims and you can't provide it, they'll assume you lacked a reasonable basis for making those statements[4][19].

Stick to factual, well-supported descriptions and avoid superlatives like "best in class" or "superior returns." These types of claims often draw extra scrutiny from regulators[19]. Instead, aim to provide balanced, straightforward information that gives potential clients a realistic view of both the opportunities and the risks.

Transparency is key when using testimonials and endorsements in marketing, and the SEC enforces strict rules to ensure compliance.

Testimonials - statements from current clients or investors - and endorsements - statements from non-clients like industry experts or professional contacts - can be powerful marketing tools. However, the SEC Marketing Rule has clear guidelines for their use. Every advertisement featuring these must disclose whether the individual is a current client or not, note any cash or non-cash compensation involved, and address any material conflicts of interest.

The SEC takes a broad view of "compensation." This includes direct payments, reduced fees, or any benefits exceeding $1,000 over a 12-month period, all of which require a written agreement.

It’s also critical to avoid cherry-picking positive reviews while ignoring negative ones. As ComplySci emphasizes:

"Financial professionals cannot 'cherry-pick' testimonials to include in their advertising. That means that when asking for a testimonial from clients, you must ask your entire book of clients – not just the ones you expect to leave positive feedback." [20]

These rules apply across all platforms, from LinkedIn recommendations to tweets. Anyone involved in creating or approving client posts must ensure proper disclosures to avoid SEC violations. Despite the updated guidance, only 5% of investment advisers have increased their use of testimonials, likely due to the complexity of compliance. [20]

Additionally, it’s essential to confirm that individuals compensated for testimonials meet SEC eligibility standards. For example, those with disciplinary histories that disqualify them cannot participate. Firms must also maintain detailed records of all testimonial agreements and conduct periodic checks to ensure third-party promoters are providing the required disclosures.

These requirements tie into the broader documentation standards for all marketing materials, including performance and rating disclosures, which are addressed in the next sections.

Third-party ratings can boost your firm's reputation, but they come with strict disclosure requirements under the SEC Marketing Rule. A third-party rating refers to any ranking or evaluation of your firm provided by an independent entity that regularly offers such ratings as part of its business.

Whenever you use a third-party rating in your advertisements, you must clearly and prominently include four critical pieces of information:

The SEC emphasizes these points, stating:

"An advertisement may not include any third-party rating, unless the investment adviser... Clearly and prominently discloses... (i) The date on which the rating was given and the period of time upon which the rating was based; (ii) The identity of the third party that created and tabulated the rating; and (iii) If applicable, that compensation has been provided directly or indirectly by the adviser in connection with obtaining or using the third-party rating." [5]

In addition to disclosures, you must ensure the rating was prepared fairly. This means verifying that any surveys or questionnaires used to generate the rating allowed participants to provide both favorable and unfavorable responses without bias. The SEC Division of Examinations is particularly focused on whether these tools were designed to produce unbiased results. As Scott H. Moss and Yvette Yun from Lowenstein Sandler LLP note:

"whether an adviser had a reasonable basis for believing that questionnaires or surveys used in the preparation of a third-party rating 1) made it equally easy for participants to provide favorable and unfavorable responses, and 2) were not designed or prepared to produce a predetermined result." [21]

To stay compliant, ensure these disclosures are easy to spot in your advertisements. Maintain thorough records, including evidence of the rating's fairness and documentation of any compensation arrangements with the rating provider. These steps are essential for demonstrating compliance during SEC examinations and upholding transparency in your advertising practices.

Performance data can be a powerful tool, but it must be handled carefully to comply with SEC rules. Whether you're presenting actual results or hypothetical projections, strict adherence to SEC requirements is essential.

Hypothetical performance - such as model results, backtested data, or projected returns - requires extra caution. According to the SEC, hypothetical performance refers to "performance results that were not actually achieved by any portfolio of the investment adviser" [5]. This type of data can only be used if it meets specific criteria: it must be relevant, all assumptions and risks must be disclosed, and it should align with the financial knowledge of your audience. Additionally, it must comply with SEC disclosure rules.

The SEC further emphasizes that hypothetical performance data should only be shared with investors who have the expertise to independently evaluate and understand the risks involved [22]. This means such data is not suitable for advertisements aimed at the general public or mass audiences.

For both actual and hypothetical performance, transparency is key. Gross performance must always be presented alongside net performance, using the same time periods and calculation methods. Both sets of data should be equally prominent and formatted for easy comparison [11]. For most advertisements (excluding private fund materials), performance results should include one-year, five-year, and ten-year periods. If the portfolio hasn’t existed for ten years, results must cover its entire lifespan.

Proper documentation is crucial - not just for compliance but also for future audits. Keep detailed records of all calculation methods and assumptions. The SEC generally expects performance results to be calculated and updated within one month after the end of a calendar year. If you use model fees instead of actual fees to compute net performance, ensure records show that the model fee was either the highest fee charged to your target audience or designed so the net figures don’t exceed those based on actual fees [11]. This level of recordkeeping demonstrates compliance and prepares you for any audits or examinations down the line.

When presenting performance data, it’s crucial to avoid cherry-picking favorable results while ignoring less impressive ones. Selective disclosure not only misleads but also violates SEC rules. The SEC explicitly requires performance results to be fair and balanced. This means you can't just highlight top-performing accounts - you need to provide a full picture by including all comparable results.

If you're showcasing performance from a specific subset of investments - what the SEC refers to as "extracted performance" - you must also disclose the performance of the entire portfolio. The SEC Division of Examinations pays close attention to cases where advisers highlight results from only a portion of portfolios that share similar investment policies, objectives, and strategies as the advertised portfolio [4]. For example, if you’re emphasizing the success of one strategy, you must also show how the broader portfolio performed to maintain transparency.

The same principle applies to time periods. You can’t just focus on high-performing years while leaving out less favorable ones. It’s also essential to include recent performance data for context. The SEC requires performance advertisements to feature data updated through at least the most recent calendar year-end, and advisers are generally expected to update this information within one month after year-end [11].

Private fund advisers face additional challenges regarding Internal Rate of Return (IRR) calculations. If you exclude subscription facilities from Gross IRR, you cannot include them in Net IRR. The SEC Division of Investment Management emphasizes:

"If an adviser chooses to exclude the impact of such subscription facilities from the fund's Gross IRR, it cannot then include them in the Net IRR" [11].

Using inconsistent methodologies like this creates misleading comparisons and violates the SEC's marketing rule.

The consequences of cherry-picking can be severe. As of September 2023, the SEC has imposed Marketing Rule sweep settlements totaling at least $2.29 million in civil penalties [23]. For instance, one RIA was fined $250,000 for violations tied to inadequate disclosures and poor documentation [13]. To avoid similar penalties, ensure your marketing materials align with your Form ADV disclosures and maintain contemporaneous records for all performance claims. Keeping your records consistent with your disclosures is a key part of staying compliant.

The SEC requires firms to keep detailed documentation to prove compliance. Whether it's an email newsletter, a social media post, or a podcast, every piece of marketing content must be archived and easily accessible for SEC examinations. This includes not just the finalized materials but also internal worksheets, memos, and approval records.

In addition to performance and disclosure documentation, thorough recordkeeping strengthens your compliance efforts. For client communications, retain records for at least five years, while testimonials and endorsements should be stored for ten years [13][15]. For oral advertisements, like podcasts or webcasts, you’ll need to keep either a written script or an audio recording [24]. Keeping accurate and comprehensive records is essential to show your adherence to SEC marketing regulations.

The SEC also emphasizes preserving records in their original format. For example, if you post on social media, capture the post along with its likes, comments, and shares, as these interactions reflect user engagement [24][25]. Tiffany Magri, Senior Regulatory Advisor at Smarsh, highlights the importance of this:

"If records cannot be retrieved and validated, compliance cannot be demonstrated" [25].

To meet the SEC’s requirements for electronic records, ensure they are stored in their original context and in a format that allows for easy searching and sorting during examinations [26]. Relying on standard email clients or inadequate storage methods can lead to lost records, which could result in penalties. In one case, a firm faced a $250,000 fine due to insufficient recordkeeping [13].

To stay compliant, document everything - from your decision-making process (like internal approvals and disclosure reasoning) to the final marketing product. This level of detail not only demonstrates "reasonable care" but also shows SEC examiners that compliance was a priority from the outset [24][15]. Using dedicated archival systems can help ensure your records are secure, retrievable, and meet all regulatory standards.

In New York, financial firms must adhere to state-specific laws in addition to federal regulations. Simply following SEC compliance isn't enough. Under Section 402-a, New York enforces its own strict advertising rules, which apply to industries like virtual currency businesses, mortgage brokers, and mortgage bankers.

State law requires businesses to include specific disclosure statements in their advertisements. For instance:

Additionally, mortgage-related ads must include the company’s name and a street address for at least one office [28][29].

Recordkeeping Requirements

New York law also has strict rules about retaining advertising materials. Virtual currency firms must keep records, including website captures documenting material changes, for at least seven years. Mortgage-related advertisements must be retained for two years, though the longer timeframe applies if both rules overlap [27][28][29][30]. Maintaining detailed records not only ensures compliance but also strengthens a firm’s overall regulatory standing.

Penalties for Non-Compliance

Failing to meet these requirements can lead to serious consequences, such as license suspension, revocation, or termination. Firms may also face financial penalties and late fees, particularly for severe violations or attempts to hide non-compliance [32].

Advertising Guidelines for Mortgage Products

Mortgage advertising in New York comes with additional restrictions. Avoid terms like "immediate approval" or "immediate closing" for loans. Clearly disclose any prepayment penalties, and only promote products that are realistically available to a reasonable number of qualified applicants on the ad's publication date. Mortgage brokers must also clarify in their ads that they arrange loans with third-party providers rather than funding the loans themselves [29][31].

New York firms must navigate both federal and state marketing regulations to stay compliant. The SEC's updated framework introduces a "unitary framework" that requires firms to follow all its provisions without exception [8][7]. This principles-based approach emphasizes thorough documentation and consistent decision-making [7][4]. These stringent requirements form the foundation for the practical tips discussed earlier.

Building a compliant infrastructure is no small task, requiring significant time and resources. For example, creating backup files to support every material claim in an advertisement can demand extensive internal effort [6]. Firms need "objective and testable means" to ensure compliance, such as pre-clearing advertisements and maintaining detailed, contemporaneous records [4]. For businesses allocating 20% or more of their revenue to marketing, handling this workload internally may become overwhelming [13].

To address these challenges effectively, working with a specialist can make a big difference. Given the resource-intensive nature of compliance, firms like Visora offer solutions that simplify processes and reduce risks. Visora partners with U.S.-based financial services firms to create compliant acquisition systems using strategic advisory and AI-supported business development. Their expertise helps firms manage complex regulatory demands while maintaining efficient marketing operations, all without increasing legal costs or expanding in-house compliance teams.

As regulations continue to evolve - especially with the growing prominence of state-level requirements alongside federal rules [8] - firms that build proactive compliance systems now will be better equipped to adapt. Whether through internal efforts or external partnerships, taking these steps today can help avoid the financial and reputational risks associated with non-compliance. Proactive measures will position firms to handle future regulatory changes with confidence.

The SEC Marketing Rule mandates that testimonials and endorsements come with clear and prominent disclosures to promote transparency. These disclosures should clarify whether the testimonial represents the genuine opinion of the individual and if any form of compensation or incentive was involved in the endorsement.

Firms are also responsible for ensuring that these disclosures are accurate and not misleading, aligning with the rule’s standards for fairness. Properly handling these requirements is key to maintaining trust and steering clear of regulatory challenges.

The SEC describes an advertisement as any direct or indirect communication designed to promote an investment adviser’s services to more than one person. This definition also applies to communications directed at a single individual if they include hypothetical performance data. However, live, unscripted oral communications - like one-on-one conversations that aren’t preplanned - are typically not considered advertisements.

Recognizing this distinction is key to staying compliant. Materials that fall under the "advertisement" category must adhere to specific SEC rules and standards. Making sure your communications meet these guidelines can help steer clear of regulatory complications.

Financial firms in New York are required to adhere to the SEC's updated marketing rule, Rule 206(4)-1, which is designed to curb misleading or deceptive advertising and solicitation practices. The rule places a strong emphasis on transparency and accuracy, demanding that all statements in marketing materials are truthful and free from misleading claims. Firms are also expected to provide clear and prominent disclosures to ensure potential clients fully understand the information presented.

When it comes to using testimonials, endorsements, or third-party ratings, the rule sets strict standards to ensure transparency. For example, firms must disclose any compensation arrangements tied to endorsements and verify that such statements comply with the rule's requirements.

To stay compliant, firms should prioritize regular reviews of their marketing materials, update internal policies to reflect the latest SEC standards, and conduct thorough staff training. These proactive steps not only help firms meet regulatory requirements but also play a key role in maintaining client trust and avoiding costly penalties.

%20(5).png)